In continuation of our FSM models update featured in yesterday’s Fund Score Overview, we will look at how the seasonal update impacted the fixed income and variable annuity models.

In continuation of our FSM models update featured in yesterday’s Fund Score Overview, we will look at how the seasonal update impacted the fixed income and variable annuity models. As a refresher, the FSM seasonal models are evaluated four times a year at the beginning of each seasonal quarter, so at the beginning of February, May, August, and November. At each evaluation, the models will sort their respective inventories by fund score, seeking to only hold those funds that possess the highest scores. The number of securities held is dependent on the model, but will typically be two or five names. For more information on the construction of the FSM models, please visit our FSM model guide.

Fixed Income Models:

Only one of our four fixed income FSM models made a change with the FSM Franklin Fixed Income ADV 2S PR4080 selling out of the Franklin Convertible Securities Fund (FISCX) and buying the Franklin Floating Rate Daily Access (FAFRX). The convertible bonds asset class was arguably the strongest area of fixed income over the last year as its high correlation to equity markets acted as a tailwind, however, that has cooled off over the past couple of months. With floating rate bonds replacing convertibles, a move higher in interest would actually be beneficial for this allocation as floating rate bonds benefit from rising interest rates. The model still maintains its exposure to emerging market debt, so there’s a 50/50 split between US and non-US exposure.

Variable Annuity Models:

Two out of the four variable annuity FSM models made changes this week. As a reminder, the variable annuity models use proxies to represent the subaccounts in the corresponding variable annuity. While we’re unable to find proxies for the entire subaccount suite of the variable annuities, we have a well-rounded lineup of proxies that represent a wide majority of the subaccounts.

The first variable annuity model that made changes was the FSM Jackson Perspective/Elite Access VA 5S PR4050 which moved out of the Oakmark International I (OAKIX) and DFA US Small Cap I (DFSTX) to buy the WCM Focused International Growth Inv (WCMRX) and the USAA NASDAQ-100 Index (USNQX). These trades match the overarching theme established in yesterday's model review, as many models moved out of small caps and value in favor of large caps and growth. The model is now overweight large caps and growth names, with high exposure toward technology.

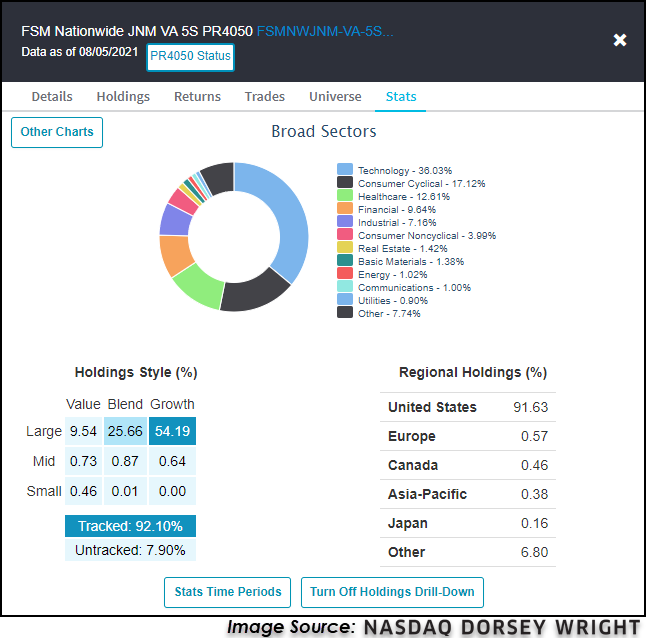

The second variable annuity model that saw changes was the FSM Nationwide JNM VA 5S PR4050 which turned over three funds. The model moved out of two mid-cap funds and one all-cap fund while buying three large-cap funds, leaving over half the exposure to be focused on large-cap growth. The model now overweights technology at 33.03% and consumer cyclicals at 17.12%. Just like the Jackson Perspective model, we see the overarching theme of the broader FSM model update highlighted once again in these changes. Large caps and growth are replacing small caps and value, which we have touched on quite frequently over the last few weeks. Complementary to the benefit of using rule-based models to make decisions and trades, we can also use them to help identify changes in market trends. Using the Asset Class Group Scores page in conjunction with the FSM models, we have a variety of methods to stay on top of market trends and changes.