As we do periodically, today we revisit the debate of active vs. passive management with updated rankings through the end of the second quarter.

As we do periodically, today we revisit the debate of active vs. passive management with updated rankings through the end of the second quarter.

Supporters of passive management assert that active managers cannot consistently outperform a passive benchmark and therefore investors are better off to invest in lower-cost index funds. Meanwhile, those in the active camp maintain that through their analysis and expertise active managers can produce persistent alpha.

The key determinate of which strategy, active or passive, is superior is market efficiency. Market efficiency describes the degree to which asset prices quickly and rationally adjust to reflect new information. In a highly efficient market, any new information is quickly incorporated into prices and therefore it is not possible to consistently achieve above average risk-adjusted returns in this type of market. Therefore, due to their lower cost, passive investment strategies are favored over active management in a highly-efficient market. In less efficient markets, on the other hand, the opportunity exists for skilled active managers to outperform passive strategies, thereby adding value for clients.

The question of active vs. passive is often framed with the premise that active or passive is always superior and often focuses on the U.S. large cap equity market, which is a natural starting point for the discussion – the large cap U.S. equity market is composed of the most well-known companies in the world and represents a large portion of many retirement portfolios. However, if we stop there we ignore what should be an obvious and fundamental element of the discussion – the various markets around the globe are not all equally efficient. The very fact that U.S. large cap companies are the most visible and researched firms in the world suggests that the U.S. large cap equity market is likely to be more efficient than its less-well-known counterparts!

Although it may appear largely academic, the active vs. passive debate has real-world implications for you as an advisor. First and foremost, you want to do what is in the best interest of your clients to help them achieve their financial goals. So, if active management really does not add value, and you will best serve your client by using passive funds to reduce expenses, then so be it. On the other hand, utilizing only passive funds eliminates one of your value propositions as an advisor – evaluating and selecting funds – and removes any possibility of outperformance. Therefore, we’ll examine several different markets individually to get a feel for which are the most efficient, and therefore likely favor passive management, and which are the least efficient, and therefore provide the greatest opportunity for active managers. The tables below show the rolling five-year return rankings of several well-known indices (representing passive management). If the index ranks in the top two quartiles, then it outperformed most managers within the peer group during that period. Conversely, if the index ranks below the 50th percentile, then most active managers in that universe outperformed the benchmark.

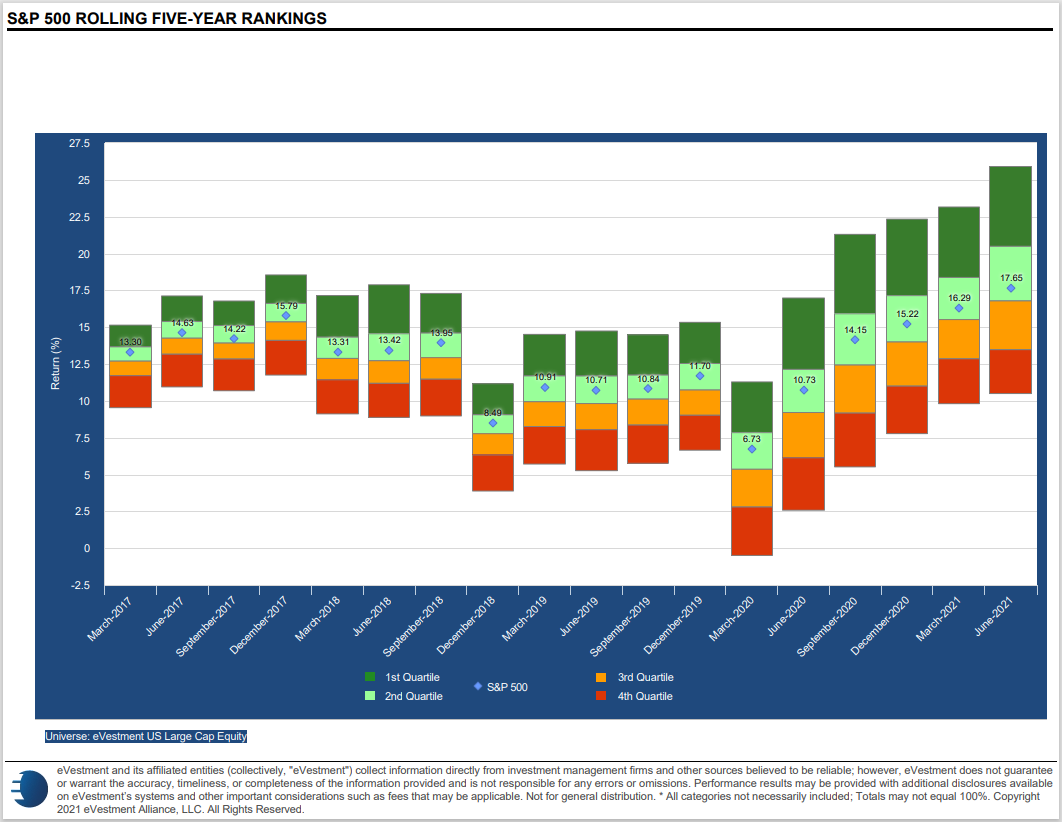

US Large Cap Equity

While there have been short periods, like the first quarter of 2021, during which the S&P 500 SPX has underperformed the average active manager, over longer periods, active managers have clearly struggled to outpace the passive benchmark. Over every rolling five-year period in our lookback window, the S&P has ranked above the 50th percentile. This does not rule out the possibility that individual mangers have consistently outperformed the index, but, in each time period the S&P has outperformed the majority of active managers. Put another way, if we had two hypothetical portfolios, one that held the S&P and one that randomly selected an active manager each period, we would expect the S&P portfolio to outperform.

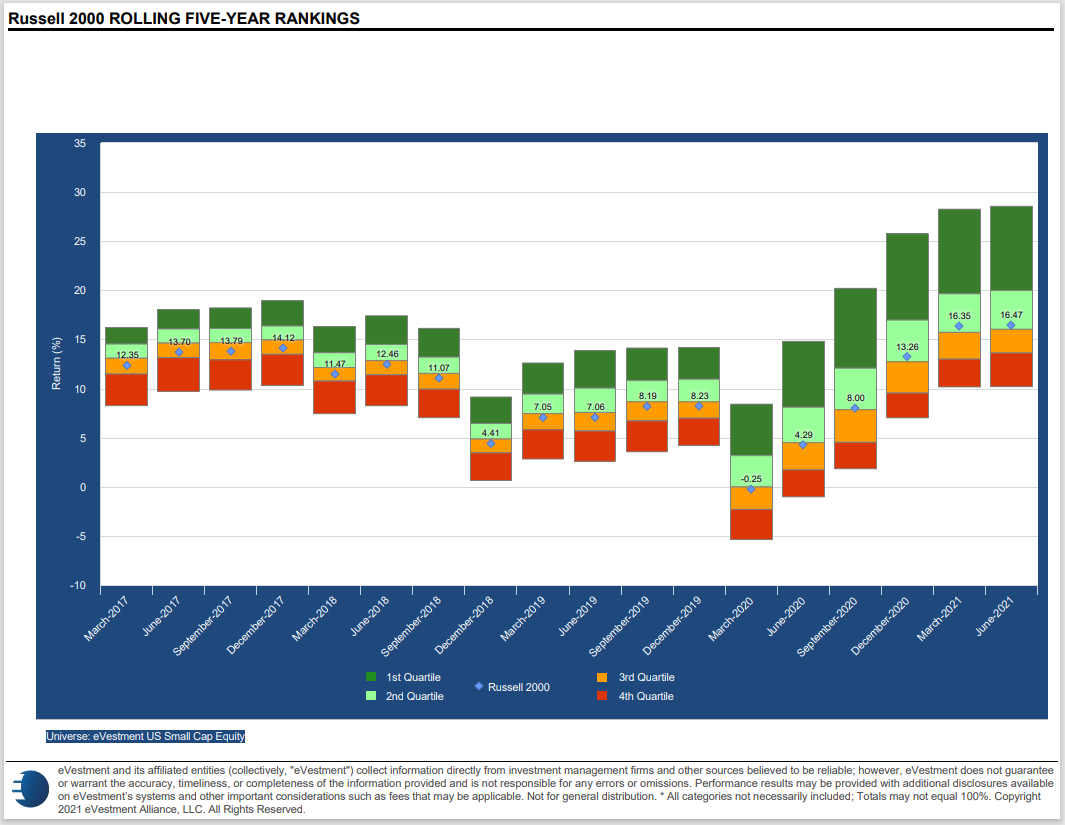

US Small Cap Equity

Anecdotally, we have heard that 2021 has been challenging for active small cap managers amid the rallies by Gamestop GME, American Entertainment Holdings AMC, and other stocks with weak fundamentals that were generally eschewed by professional managers. This may, at least partially, explain why we have seen the benchmark climb above the 50th percentile in the most recent time periods, while it had ranked in the third quartile during most periods ending before 2020. At this juncture, it would be hard to say whether active or passive management is clearly favored. The recent underperformance by active managers is something to keep an eye to see if it is merely a short-term trend confined to an unusual market environment or if develops into something more long-term.

Developed International Equity

The passive EAFE index finished below the 50th percentile in almost every five-year period shown indicating that on average active management has been able to add value. Based on the historical evidence, we would expect to benefit by utilizing active management in the space as opposed the passive benchmark.

Emerging Market Equity

Similar to what we saw in the small cap space, the MSCI emerging markets index has finished above the 50th percentile over the last several time periods after ranking in the bottom two quartiles in many periods prior to 2020. Once again, this is a development worth keeping an eye on to see if it is short-term in nature or persists to become a long-term trend.

US Core Fixed Income

The US aggregate index ranks squarely in the bottom quartile across most time periods in our lookback period leaving little doubt that most active managers outperform the benchmark. It is worth noting that there are number of ways that active fixed income managers can subtly alter their portfolios – e.g. reducing Treasury exposure and increasing corporate exposure – to gain a return advantage over the index. But doing so also increases the risk (credit risk in this example) of the portfolio. The point being that while most US core fixed income managers are outperforming the benchmark, many may be doing so by marginally increasing risk.

Global Fixed Income

As with domestic fixed income, the rolling five-year rankings also show consistent outperformance by active managers.

Ultimately, whether active or passive management is better comes down the individual market in question. There are several markets in which active managers show consistent outperformance. There are also more efficient markets, like US large cap, in which active managers have struggled to outperform the index. Making a market-by-market assessment when deciding whether to employ an active or passive strategy provides us the opportunity to save money on fees by utilizing passive strategies in highly-efficient markets and add value by identifying inefficient markets and selecting skilled active managers who can generate superior returns.