The Magnificent Seven has struggled to start the year, is it time to give up on the mega cap stalwarts?

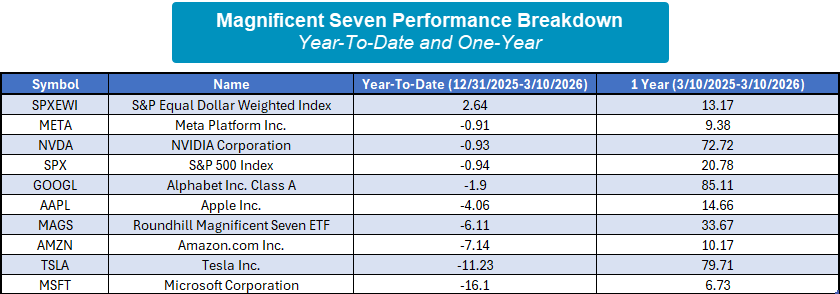

The “Magnificent Seven” has been a dominant force in the market for years, consistently carrying the cap-weighted indices higher while equal-weighted schemas languished. The last few months have seen that trend change as the S&P 500 Equal Weight Index (SPXEWI) outpaces the S&P 500 Index (SPX) by roughly 3.5% year-to-date (2.64% versus -0.94%). The Magnificent Seven stocks, a large portion of the SPX, have really struggled this year relative to the SPXEWI. Using the Roundhill Magnificent Seven ETF (MAGS) as a representative, MAGS is down more than 6% this year with every Magnificent Seven stock in the red year-to-date. However, over the last year, MAGS is up 33.67% versus 13.17% for the SPXEWI and 20.78% for the SPX. So, we’ll need to see a longer or more severe period of underperformance before the evidence starts to pile up against the Magnificent Seven. One interesting point is the dispersion within the Mag Seven stocks over the last year with Alphabet (GOOGL), NVIDIA (NVDA), and Tesla (TSLA) each gaining over 70% while Meta (META) and Microsoft (MSFT) returned less than 10%.

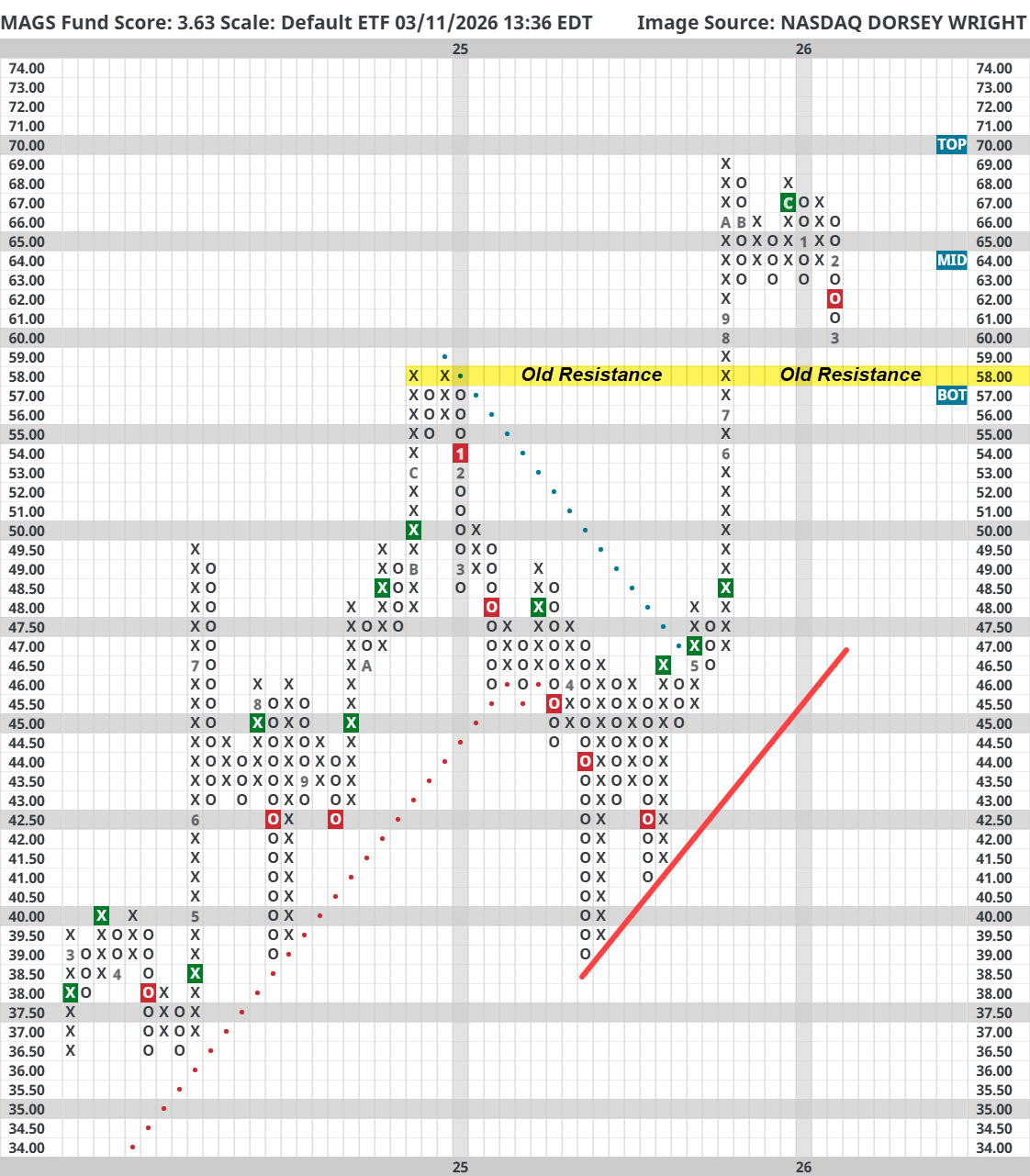

Focusing on MAGS’s chart action, the fund broke a quadruple bottom in February, its first sell signal since April 2025. The immediate concern at first glance is the lack of established support nearby. Prior resistance at $58 may act as support but below that there is no established support until $46.50. The fund score for MAGS is still in acceptable territory at 3.63, but it does have a 2.21 negative score direction, which speaks to its decline in relative strength over the last few months. While these handful of mega cap names have slowed down, many are still in strong standing on an individual basis. When looking to trim or exit one of the Mag Seven names that are likely in at least a few of your clients’ portfolios, be sure to check on the individual technical pictures for each even if the overall group has slowed down. Secondly, the strong performance of these handful of names may have led portfolios to having an outsized allocation. So, this could be a good opportunity to reallocate portfolios towards emerging areas of relative strength without completely selling out of the Mag Seven. If these mega caps continue to weaken, then more changes will be needed.