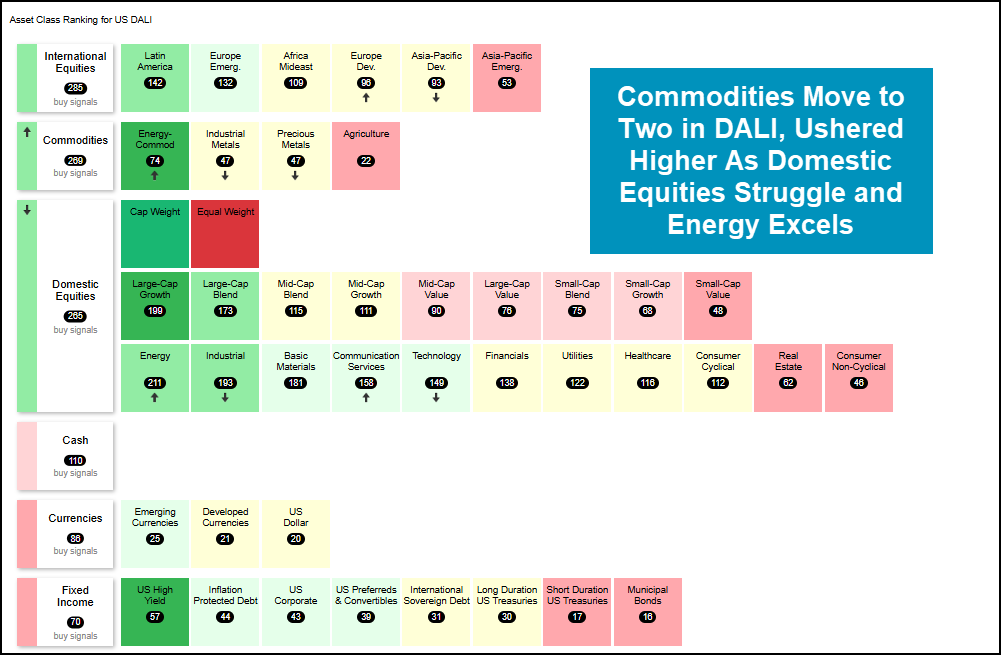

Energy focused moved into the 2nd position within the DALI rankings. We cover what that might mean for you and what charts you need to be watching as we move through March

Recent events have ushered in lots of price movement worth watching… and perhaps more importantly said price action has stemmed from parts of the markets that have been dormant for quite some time. As usual, unrest in the middle east has sent energy prices skyrocketing, seeing the price of crude climb over $100 (even hitting nearly $120 over the weekend) for the first time since 2022. This comes after the last three years have seen little to no sustained upside action for any parts of the larger energy complex, with many representatives having traded largely sideways since the start of 2023’s bull market. Of course, the rapid movement of energy’s upside has led to some notable changes in relative strength… changes we will discuss in more detail today.

The largest change on the platform most of you will see is Commodities overtaking Domestic Equites for second place within the overall broad rankings within DALI. The move marks the first instance of domestic equites sitting outside the top two rankings since June of last year when international equites, commodities (largely precious metals) and domestic equities were all vowing for the top spot. The three-way battle for first was ultimately reclaimed by domestic equities… but the move served as a reminder for technical strength outside of the core domestic space. It is worth mentioning that despite domestic equites moving lower, the top three asset classes remain relatively risk-on, while other areas like fixed income and cash have yet to see notable upticks. A general rule of thumb for those of you looking to make broader allocation changes based on the change- wait to see if this shift is “legitimate.” Take last summer’s brief bounce in top three leadership positioning as a lesson that those of you too quick to make changes can be quickly punished… especially when moving out of domestic equites which many of you benchmark to.

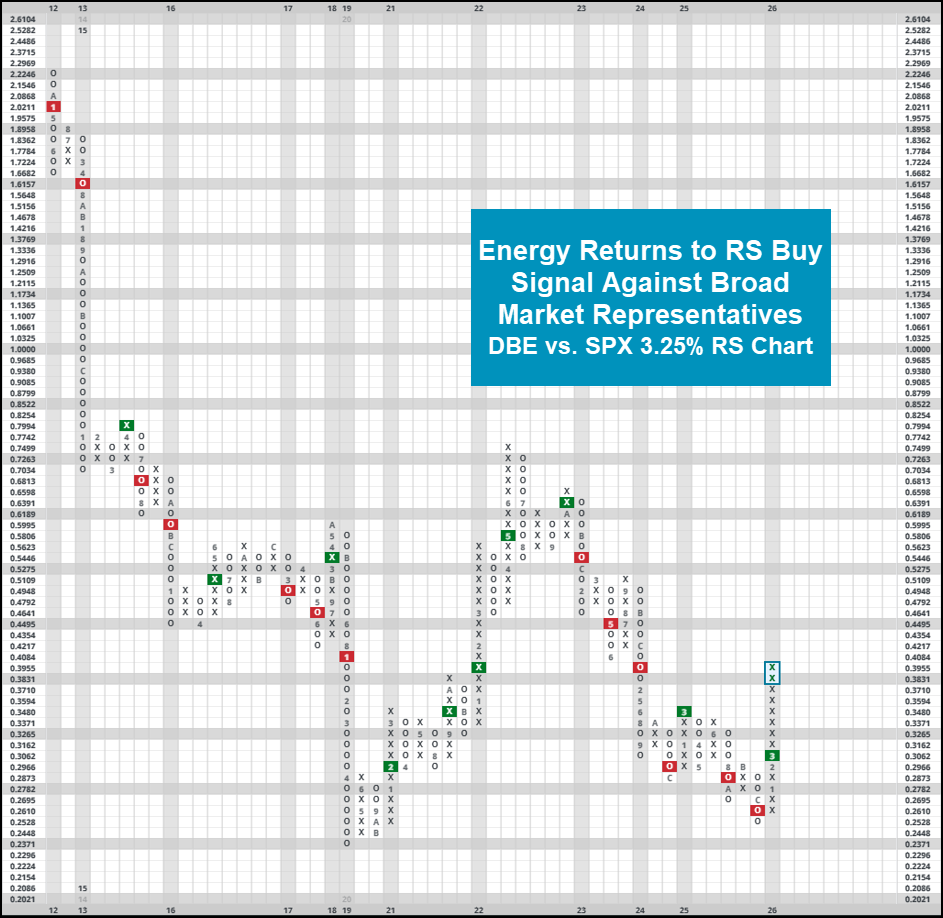

For the uninitiated, DALI is a matrix based ranking system that throws together several representatives against each other to see which members are relatively strongest. While the exact breakdown of DALI constituents is proprietary to NDW, we take care in updating/monitoring the universe to ensure every group is represented fairly. Outside of our matrix-based system, there have been several relevant relative strength relationships that have shifted in favor of energy options over the last week. Invesco Energy representative DBE (up ~50% this year) most recently returned to a buy signal against SPX, SPXEWI & NDX since the start of March. DBO (oil) & DBC (broad commodities] have seen similar RS rotations. While the shifts are certainly is quite notable, it is important to highlight the overbought nature of many of these representatives. The near 200% weekly OBOS for DBE is one of the highest readings ever, and many energy representatives sit without relevant support on their default charts for quite some way.

All of this to say, continue to exercise caution on the equity front. The drop down out of the top two positions in DALI is quite notable, but rapidly cutting domestic equity exposure in exchange for an overbought commodity space certainly carries risk. Regardless, the drop in relative strength does suggest we could continue to see volatility as we wrap up Q1 2026, so keep an eye on the charts.