As we do each quarter, today we update our U.S. and International "Smart Beta Quilts" and Factor Studies for the second quarter of 2021.

As we do each quarter, today we update our U.S. and International "Smart Beta Quilts" and Factor Studies for the second quarter of 2021. Before the term “factor investing” became commonplace within the financial community, there were two main "factors" that advisors were already using within client portfolios: growth and value. Advisors commonly used various market capitalization sizes or some form of style rotation, but beyond that, there was not a lot of access to many of the security selection processes that are available today. Over the past decade, the number of investable factors has increased significantly, thanks in large part to the proliferation of ETFs. The term "factor" is broad, and there is a healthy debate as to what exactly should fall into that category. Arguably, any indexing strategy in which securities are chosen systematically, based on measurable attributes, with a goal of producing superior returns over the asset class would qualify. Still, that covers a wide range and is a vague definition, but we can agree it goes well beyond "growth" and "value."

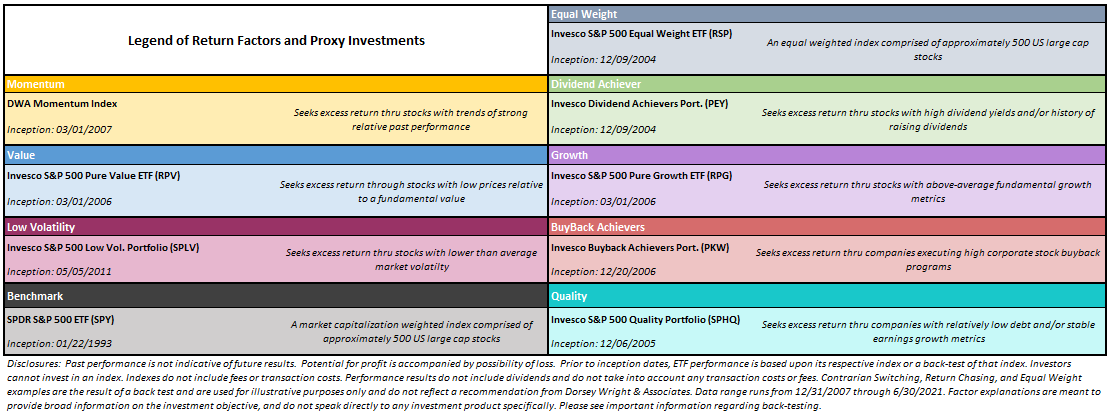

Other factors that are commonly accessible through ETFs today are momentum, low volatility, quality, dividend achiever, and buyback strategies. All of these factors are designed to pinpoint a certain investment theme within the marketplace, and systematically allocate to that theme. For instance, the “low volatility” factor is represented by the Invesco S&P 500 Low Volatility ETF (SPLV), a fund that seeks exposure to the 100 stocks with the lowest volatility in the S&P 500. Over time, most of the factors examined offer better performance than the benchmark, the SPDR S&P 500 ETF (SPY), however, no single factor ETF has been the best performer every year, or even most of the years...nor has any single factor ETF been the worst performing every year or most of the years.

Factor Return Observations (US Equities):

- Value has been the best performing factor throughout the first half of the year with a gain of 25.56%. This comes after value finished either last or second to last in each of the prior three years.

- Momentum went from the best performing factor for two consecutive years to the worst-performing factor year-to-date in 2021; momentum now shows a positive 2.14% return for the year after being in negative territory after the first quarter.

- After finishing in the bottom half of the factor rankings in 2021, buyback has been the second best performer in 2021, gaining just over 23%.

- Growth is still the best performing factor from a cumulative perspective, though it ranks seventh year-to-date.

- After a poor performance in 2020, the contrarian switching strategy has been the best performing "strategy" in 2021, while "return chasing" has been the worst performer.

How do I use this information to build a portfolio around factors?

Our goal with the research above is both to illustrate the range of factors that are available and also the necessity of being disciplined in applying these factors over time as we want to promote "good behavior", as it relates to any investment process or product. This is perhaps the most important observation from the data above: We've illustrated the outcomes generated by a few common behaviors using the same investment universe, and the outcomes vary dramatically! There are the "buy and hold" outcomes, which show growth as the best performer, but we also know inherently what comes with a buy and hold commitment to only growth. While not visible above, 2000-2002 were tough years for that factor, tougher than many could endure in fact. Another approach that we illustrate is to simply equal weight all seven of the individual factors in a portfolio and rebalance that portfolio once a year. Additionally, we looked at the hypothetical behavior of buying the best performing factor from the previous year and holding that factor for the entire next calendar year. For our purposes, we label this “Return Chasing,” and while no portfolio manager markets themselves this way exactly, it is an emotional bias that creeps into many investors' psyches.

This "Return Chasing" portfolio tracks a hypothetical investor who sees that momentum was the best performing factor in 2020, and then just owns that factor for 2021. This strategy worked out well in 2020 and there have been a few other years where the return chasing worked out, such as when value was the best performer in back-to-back years from 2012 to 2013. However, even though it has worked out well in a few instances, on a cumulative basis, return chasing has been the worst “strategy” and has massively underperformed the contrarian strategy and an equal-weighted basket of the factors. The factors themselves are not the problem, as most create substantial alpha relative to the market. However, bad behavior can create bad returns out of good products, and constantly chasing last year's best performing factor is an example of bad behavior.

The opposite of return chasing is the contrarian approach, which hypothetically buys the worst-performing factor from the previous year and holds it for the subsequent calendar year. The “Contrarian Switching” portfolio illustrates what is missed when an investor dumps a factor for having a bad year, and this strategy outperformed both cap-weighted and equal-weighted benchmarks over the study period! A good stock can become a bad stock and may remain a bad stock for a long time. A good factor is much less likely to remain perennially out of favor. A good factor should have a process of systematically eliminating bad stocks at some point and should return to favor as a result. Each factor illustrated above is available through an ETF, or multiple ETFs because they have been vetted through research and real-life portfolio management applications, which provides some confidence that periods of underperformance should not become perpetual underperformance.

This tells us that lagging years for a good investment factor have commonly been better-than-average entry points. In 2016, momentum had a rough go of it, which was the first time during the lookback period that it was the worst-performing factor. In the following year, it was the second-best performing factor behind growth, and these were the only two factors to outperform the benchmark. 2017's worst-performing factor (shown above) was the "Dividend" factor, which we represent with a Dividend Achiever portfolio (PEY), which is weighted based upon yield. The long-term returns for this fund are heavily weighted toward dividends and so the price return of the fund is perhaps less representative of the outcome than with other factor-based products. In 2018, we did not see much of a "mean reversion" as PEY was near the bottom of the pack again. Value also had a rough go of it during 2018, which was followed by underperformance in both 2019 and 2020. As a result, the "Contrarian Switching" approach lagged in those years. However, through the first six months of 2021 we have seen somewhat of a return to form for the Contrarian Switching strategy, as value went from the lowest-ranked factor in 2020 to the best so far this year.

These strategies can also be applied to factor representatives from international equities, which, as we can see below, demonstrate similar tendencies to their domestic counterparts.

Factor Return Observations (International Developed Equities):

- Buyback was the best performing international equity factor through the first six months of the year; if it finishes the year in first place, it would be the first time since 2017. Despite its lack of "wins" over the last few years, buyback remains the top international factor on a cumulative basis.

- While momentum has lagged domestically, it has performed well in international markets this year, ranking third behind dividend achievers

- After being the worst performing factor during the first quarter of 2021, growth moved out of the basement in Q2; low vol is now the worst performing factor year-to-date after also lagging all other factors in 2020.

- Unlike the US, the contrarian switching strategy has lagged internationally in 2021, while return chasing has been the best performing "strategy" thanks to momentum's stronger relative performance outside the US.