We examine several different markets to find out which are the most efficient and which are the least efficient. In order to get an idea of the level of efficiency, we will take a look at rolling five-year return rankings to see how several of the most well-known indices (representing passive management) have performed.

In a prospecting article from May we looked at the relative performance of active and passively-managed funds during the volatile months of March and April, a period that theoretically should have favored active managers. With two quarters of 2020 officially behind us, we thought this would be an opportune time to take a look at the longer-term relative performance of these strategies.

Proponents of passive management insist that active managers cannot consistently outperform a passive benchmark and therefore investors are better off to invest in lower-cost index funds. Meanwhile, those in the active camp maintain that through their analysis and expertise active managers are able to produce persistent alpha. The question of active vs. passive is often framed with the premise that active or passive is always superior and focuses largely on the U.S. equity market. However, all markets are not the same and so we should examine the merits of each style on a market-by-market basis instead of taking a one-size-fits-all approach.

The active vs. passive question has special implications for you as an advisor. First and foremost, you want to do what’s best for your clients to help them achieve their financial goals. So, if active managers don’t add value, and utilizing passive funds in order to reduce expenses is in the best interest of your clients, then so be it. On the other hand, utilizing only passive funds eliminates one of your value propositions as an advisor – evaluating and selecting the best funds for your clients – and removes any possibility of outperformance. Therefore, today we’ll examine several different markets in order to find out which are the most efficient and which are the least efficient. In order to get an idea of the level of efficiency, we will take a look at rolling five-year return rankings to see how several of the most well-known indices (representing passive management) have performed.

As mentioned above, the active vs. passive debate often examines only large cap U.S. equities, which is a natural starting point for the discussion – the large cap U.S. equity market is composed of the most well-known companies in the world and represents a large portion of many retirement portfolios. However, if we stop there we ignore what should be an obvious and fundamental element of the discussion – the various markets around the globe are unlikely to all be equally efficient. The very fact that U.S. large cap companies are the most visible and researched firms in the world suggests that the U.S. large cap equity market is likely to be more efficient than its less-well-known counterparts!

In addition to variation across markets, individual markets can also have different characteristics in distinct time periods. During the 10-year bull market from 2009 – 2019 active managers, especially in the U.S. large cap space, often struggled to match the performance of their benchmarks. There have been other periods in the past during which active management has underperformed passive for several years only to have the trend reverse. We cannot rule out the possibility that there have been fundamental changes to the U.S. large cap equity market which will prevent active managers from regaining superiority. However, we also cannot dismiss the possibility that over the last several years we’ve simply been in a market environment that favored passive strategies and the pendulum will swing back in favor of active.

The passive US indices (the S&P 500 SPX and the Russell 2000 RUT) have performed well on an absolute basis with both posting positive returns across almost all time periods examined. The average active manager has struggled to outperform the S&P 500, as the index did not rank below the second quartile in any of the periods shown. On the other hand, the average active manager has been able to narrowly outperform the Russell 2000 finished squarely below the second quartile all periods except for the most recent two. While it’s possible for active managers to outperform both indices, a strong case can be made for passive management in the S&P 500. However, active management has continually outperformed the Russell 2000 making a strong case for active management in the small cap space.

Moving on to the non-US equity rankings, we see that both the developed and emerging market indices rank in the bottom half of their respective universes in almost every period observed. This tells us that the average active manager in these markets has outperformed the index, adding value for their clients, and indicates that active strategies are likely to be preferable in these markets.

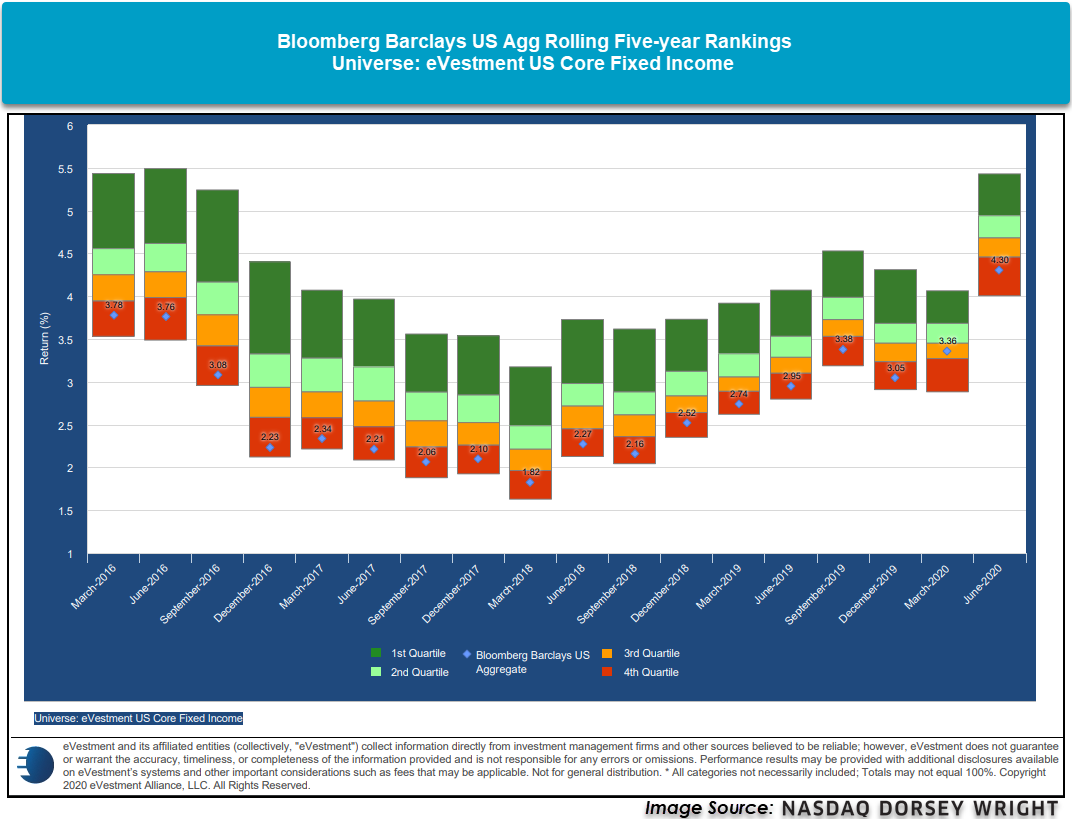

Lastly, US and non-US fixed income active managers have continuously outperformed the indices, especially within the US fixed income space. Similar to the non-US equity indices, active managers have persistently added value for their clients, and active management is likely preferable within the domestic and global fixed income markets.

So, as to which is ultimately better - active or passive - the correct answer seems to be, it depends on the market. As we’ve seen, there are several markets in which the average active manager has usually been able to outperform the index. We’ve also seen there are more efficient markets in which active managers have struggled to outperform the index. Making a market-by-market assessment when deciding whether to employ an active or passive strategy for your clients will allow you to save them money by utilizing passive strategies in efficient markets and add value by identifying inefficient markets and selecting skilled managers who can generate superior returns.