Leading the way to the downside among the sectors has been Utilities, which along with notable technical developments, may be seeing a change of the guard in terms of underlying leadership themes for the sector.

While there is still time left, May’s trading has not been too kind to sectors outside of Technology. While tech is up more than 12% so far through May, based on the State Street Technology Select Sector SPDR Fund (XLK), the remaining ten SPDR funds are down an average of 71 basis points. Leading the way to the downside among the sectors has been Utilities, which, along with notable technical developments, may be seeing a change of the guard in terms of underlying leadership themes for the sector.

The State Street Utilities Select Sector SPDR Fund (XLU) has fallen more than 4% during May (thru 5/14), and after reversing down into Os on the default trend chart during last Thursday’s (5/7) trading, this Wednesday’s (5/13) trading led to a second sell signal, with a double bottom break at $44.50. The breakdown follows another failed attempt to penetrate resistance within the $47 range, and brings the chart down to test the bullish support line.

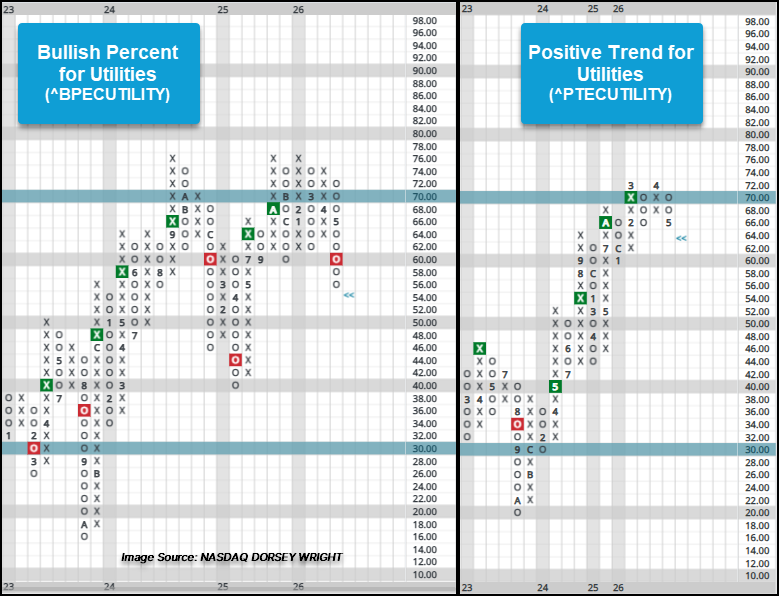

While XLU witnessed a second sell through continued consolidation within the mid $40s, individual utilities names saw a notable shift in those maintaining point and figure buy signals as the broader sector bullish percent (^BPECUTILITY) fell from the mid-60s to the mid-50s, marking the lowest level in roughly 12 months. The subsector bullish percent indicators for electric utilities (^BPEUTI) and gas utilities (^BPGUTI) similarly fell to near or below 12-month lows with readings in the upper 50s and lower 60s during this week’s trading. The long-term positive trend indicator for the broader sector (^PTUTILITY) reversed down to Os to 66% following Wednesday’s (5/13) trading. Though the readings of these intermediate- to long-term indicators have fallen, most still remain above the 50% threshold, suggesting the majority of stocks continue to maintain a buy signal and positive trend. But while utility investors closely monitor those indicators, notable developments within an underlying theme have begun to occur.

While artificial intelligence (AI) has been among, if not the main, theme for the past few years or more, nuclear energy has been a sub-theme that has garnered attention from retail to institutional investors, with AI companies themselves partnering with specific utility providers to power data centers.

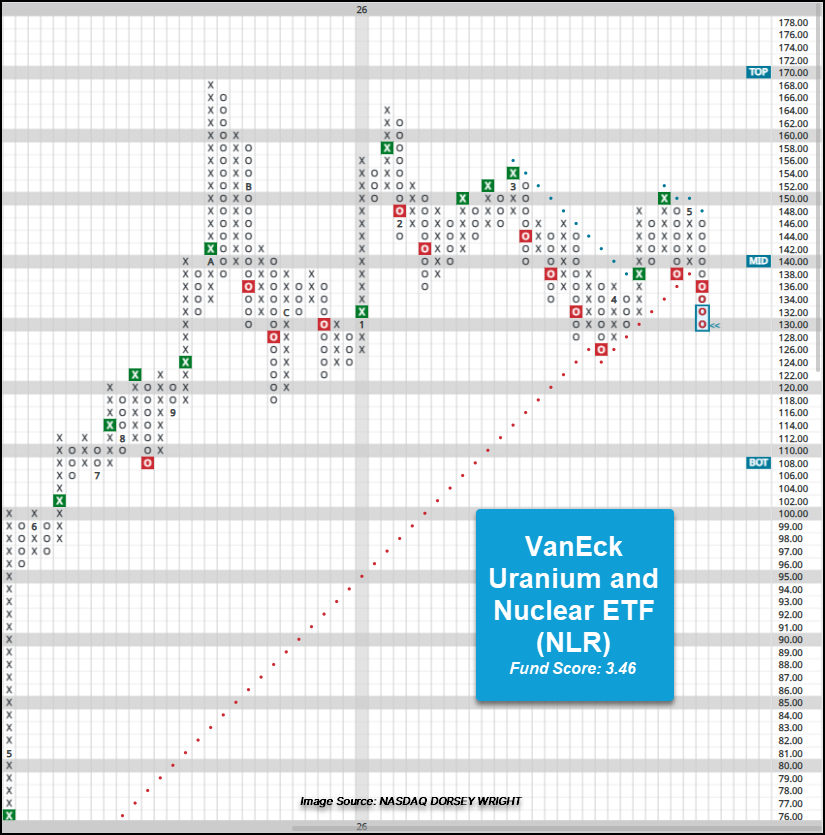

Among the more popular ETFs targeting the nuclear energy theme is the VanEck Uranium and Nuclear ETF (NLR). Similar to XLU above, this week’s trading brought a second sell signal for the fund, but along with the sell signal, NLR also witnessed a violation of its bullish support line, shifting the long-term trend to negative. While the market RS chart has been in Os since February, the peer RS chart for NLR shifted into Os during this week’s trading and brings both charts to within at least a box or two of a potential RS signal change, highlighting not only near-term relative weakness by the fund, but the potential shift in long-term weakness as well. NLR maintains an acceptable fund score of 3.46 as of Wednesday’s (5/14) close, but should additional relative weakness show, the score could see further deterioration. On the trend chart, long-term support still remains in the upper $110s to $130 range, but should these levels be violated, it would break the fund out of a range of consolidation that has been prevalent since Q4 2025.

Funds like XLU and NLR have long-term support intact, but some of the original darlings of the AI-nuclear theme have witnessed notable technical breakdowns during this week’s trading. The aforementioned “original darlings” are traditional utility companies providing nuclear energy, but some of the shift in theme has been diverted from the large utility companies to specialized companies’ development of micro nuclear or energy solutions that can be deployed on-site at data centers. Much of the shift has been driven by companies building data centers seeking reliable solutions to their immense energy needs and less reliance on the current electrical grid.

While there are a few good examples that could be used for conveying those names leading and lagging within the AI nuclear sub-theme, recent trading within NRG Energy (NRG) and Bloom Energy (BE) stands as a prime candidate. To briefly rewind two years though, it is worth noting that NRG Energy was one of the largest suppliers of nuclear energy to the shared power grid by consumers, while Bloom, a maker of micro fuel cell for power generation, was trading around $10 and fairly unknown to those just dipping their toes into the tangent AI theme within nuclear energy. NRG rallied through 2024 and front half of 2025 before stalling in the mid-$100 range. Trading over the past couple of weeks has witnessed NRG move into a negative trend and breakdown out of the phase of consolidation that has persisted for roughly 11 months. Meanwhile, BE similarly rallied in 2024 and 2025, but rather than consolidating and breaking down in 2026 like NRG, BE has continued higher, marking a new all-time chart high above $300 this week. The trend change this week brought NRG down to a 2 for 5’er in technical attribute rating, while BE has maintained a 5 technical attribute rating since mid-April.

The shift within the nuclear AI theme in 2026 has been less focused on the large utility companies with nuclear power plants that were the original darlings within the theme like NRG, Vistra (VST), and Constellation Energy (CEG), and to those companies like Bloom (BE), Oklo (OKLO), and Nano Nuclear (NNE). Even among the new wave of companies garnering attention, BE is currently the only 5 TA rated stock and is trading at an overbought level currently. With the level of price volatility within some of the aforementioned stocks, it does highlight the changing over time of how stocks within a sector can be perceived; these are not the coal and hydroelectric utility dividend payers your grandfather or father may have retired with. While exposure to the broader sector is likely an equal or underweight position within portfolios, shifts within these nuclear utility names have begun to have major effects on the broader sector, one that has historically been associated with defensiveness and less volatile price movement. The recent changes within the AI nuclear sub-theme within utilities and breakdowns within some of the original darlings shown above have brought the broader sector to an intriguing inflection point that will be worth monitoring moving forward.