Fixed income sits at a crossroads, facing duel technical and fundamental forces that could push it higher or lower. Which outcome appears most likely, and how should investors navigate the group?

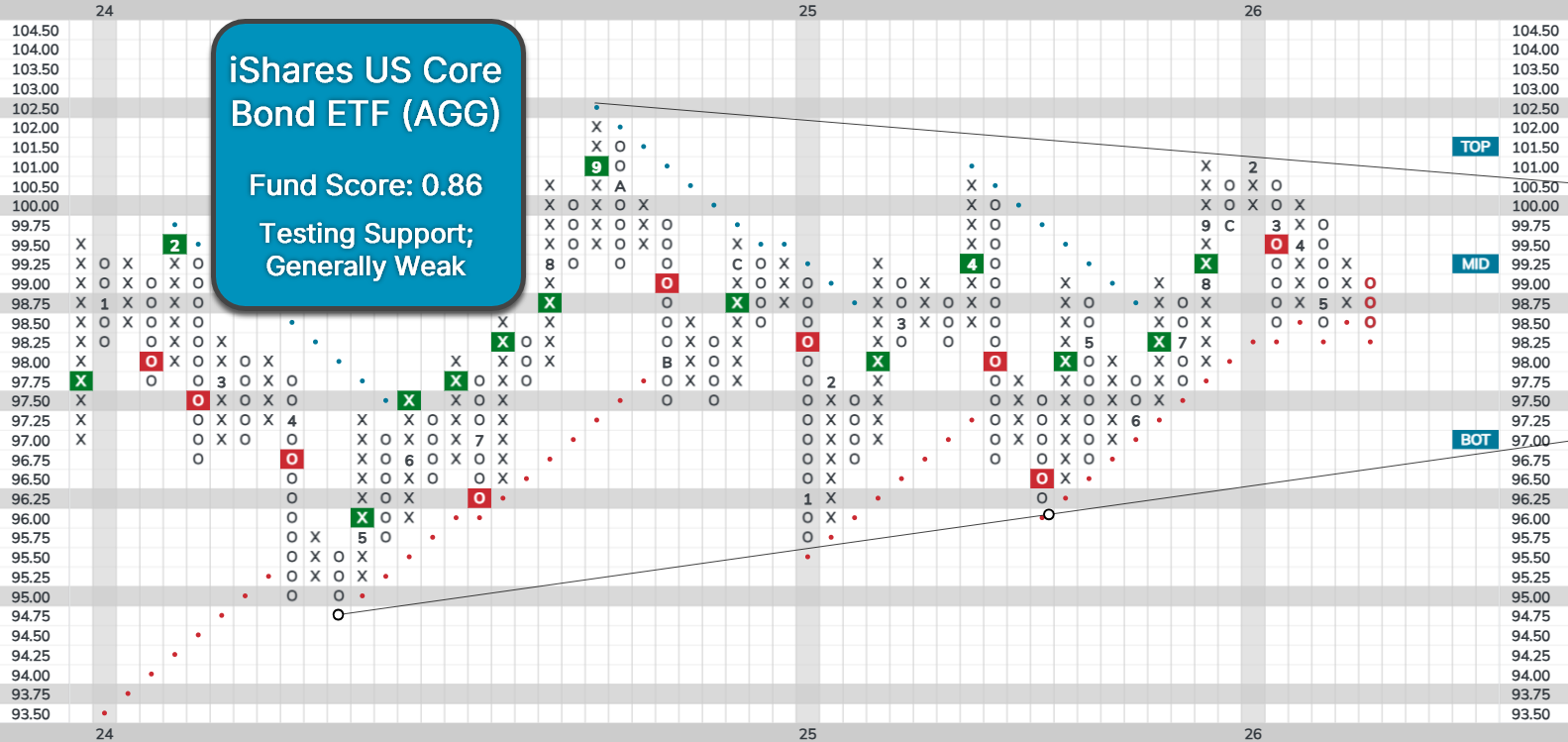

Fixed income sits at a crossroads. The asset class has gone virtually nowhere over the past five years, with the iShares US Core Bond ETF (AGG) up a mere 70 basis points, even when including its yield. The past two years have been even more uneventful, as AGG has traded within a narrow range of $95 to $102, with that range gradually tightening. Regardless of which way bonds end up moving, AGG reversing to new heights or breaking through support would be a significant development, with it likely to continue trending in that direction. Given this uncertainty and its importance, which outcome appears most likely, and how should investors navigate the group?

The Bull Case

On one hand, interest rates could fall over the next year if Fed Chairman Warsh pushes the organization towards a less restrictive policy or advocates for further rate cuts. Meanwhile, AGG sits right above significant support at $98.50, so it’s possible bonds reverse higher from current levels and finally break out to the upside. Given the significance of overhead resistance, any movement above $ $102.50 would be a notably bullish development for the asset class. Even on a total return basis, AGG has yet to recover from its 2020 peak, but a move back to those highs could mark the start of a new era for bonds.

The Bear Case

On the other hand, inflation remains persistent, with recent readings adding to pessimism. CPI rose 3.8% from April 2025, marking its highest reading in nearly three years. Even excluding food and energy, PCE inflation—the Fed’s preferred measure—sat well above the 2% target at 3.2% in March, underscoring that inflationary pressures extend beyond energy prices. The expected Fed Funds rate for the end 2026 has shifted higher by the equivalent of three full cuts, rising from 2.94% in November 2025 to 3.73% today.

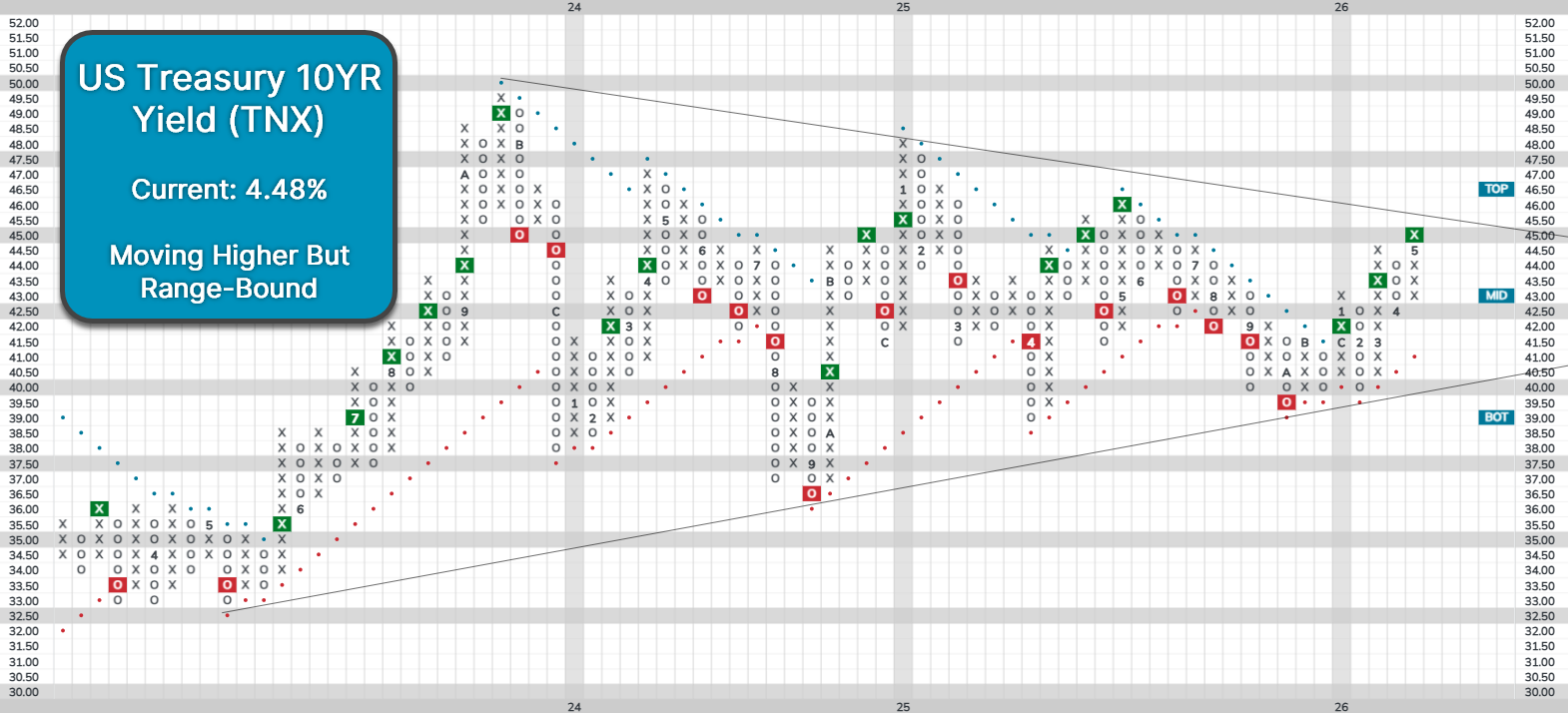

These factors have also led to notable technical changes. AGG moved back to a sell signal in March, and any further downside would return it to a negative trend for the first time in a year. Additionally, the 10-year Treasury yield (TNX) is back near 4.5% after registering its third consecutive buy signal, with “run-it-hot” policies from the administration contributing to upward pressure on long-term rates. For now, rates are likely to continue moving within their current range in the near term. However, rates will eventually break out of this range, and when they do, both technical and fundamental evidence suggest it is more likely to be a reflection of a higher-for-longer environment than declining rates.

Given the overall weakness in fixed income, with it ranking last in DALI, it makes sense to target select areas within the asset class, if investors choose to own it at all. Looking at the Asset Class Group Scores page, investors can see which subgroups remain attractive. Investors seeking more risk-on exposure could target convertibles or international bonds, as these are the only fixed income segments with average scores near or above 3. While high-yield bonds also rank well, credit spreads are near historic lows, suggesting limited upside remains. More risk-averse investors could consider inflation-protected or floating-rate securities, as they rank ahead of the broader fixed income space. Lastly, long-duration bonds may warrant an underweight given their lack of relative strength and greater downside risk if rates rise further.