While the last three years were extremely strong for both the economy and the financial sector, the start of this year has been a very different story. Given recent movement, how should we view financials and the sector's implications on the broader market.

For better or worse, there’s no such thing as a crystal ball that predicts markets. Instead, the best we have are indicators and areas of the market that are more likely to precede movement of the economy. Among the eleven major sectors of domestic equities, the financial sector is the most likely to foreshadow movement in the broader economy. While the last three years were extremely strong for both the economy and the financial sector, the start of this year has been a very different story.

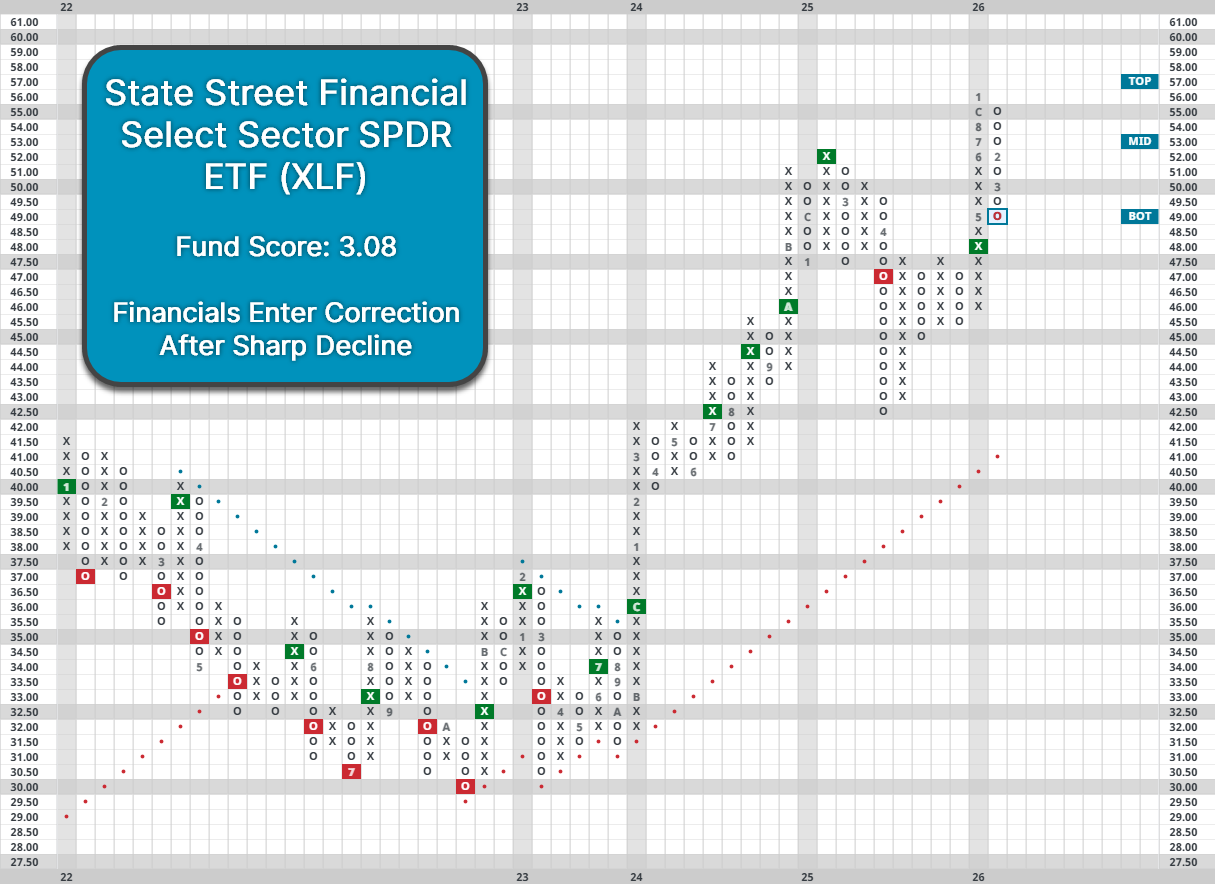

The State Street Financial Select Sector SPDR ETF (XLF) is down more than 10.8% YTD—its worst beginning to a year besides of the start of Covid since 2009. The fund is back to price levels first achieved in 2024, and its fund score has fallen to a mediocre 3.08, which is its lowest since late 2023. Meanwhile, the group is down to the middle of DALI after sitting in the number one spot as recently as last March. The broader sector has unquestionably weakened, but which areas have taken the largest hit, and are there concerning catalysts causing the decline?

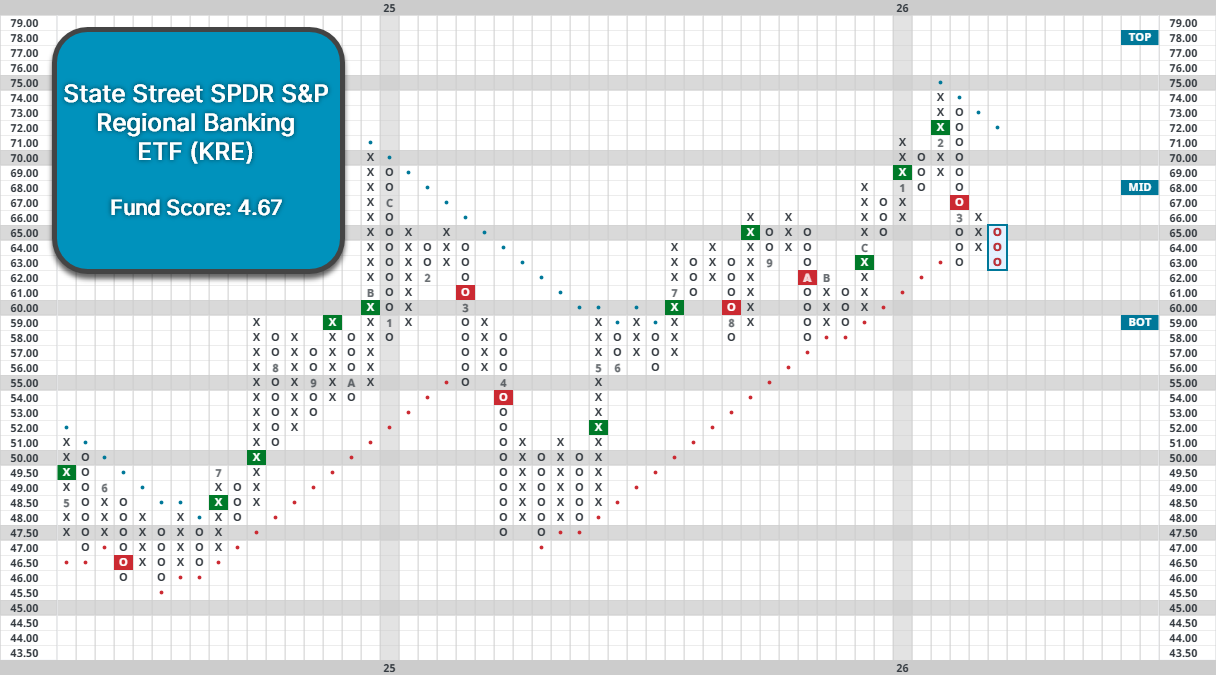

Banks have seen the most downside within financials over the last several months, and regional banks have been hit especially hard. Regional banks focus heavily on lending to small businesses, real estate developers, and local consumers, making their performance directly tied to local credit conditions and economic activity. Deteriorating credit conditions (read more below), commercial real estate woes, and consumer spending concerns have all served as recent headwinds. The State Street SPDR S&P Regional Banking ETF (KRE) is down more than 11% over the last month, moving to a negative trend for the first time since last year. While KRE holds a solid fund score of 4.67, its recent performance marks notable divergence from previous action, making it an area to watch for further weakness in the coming months.

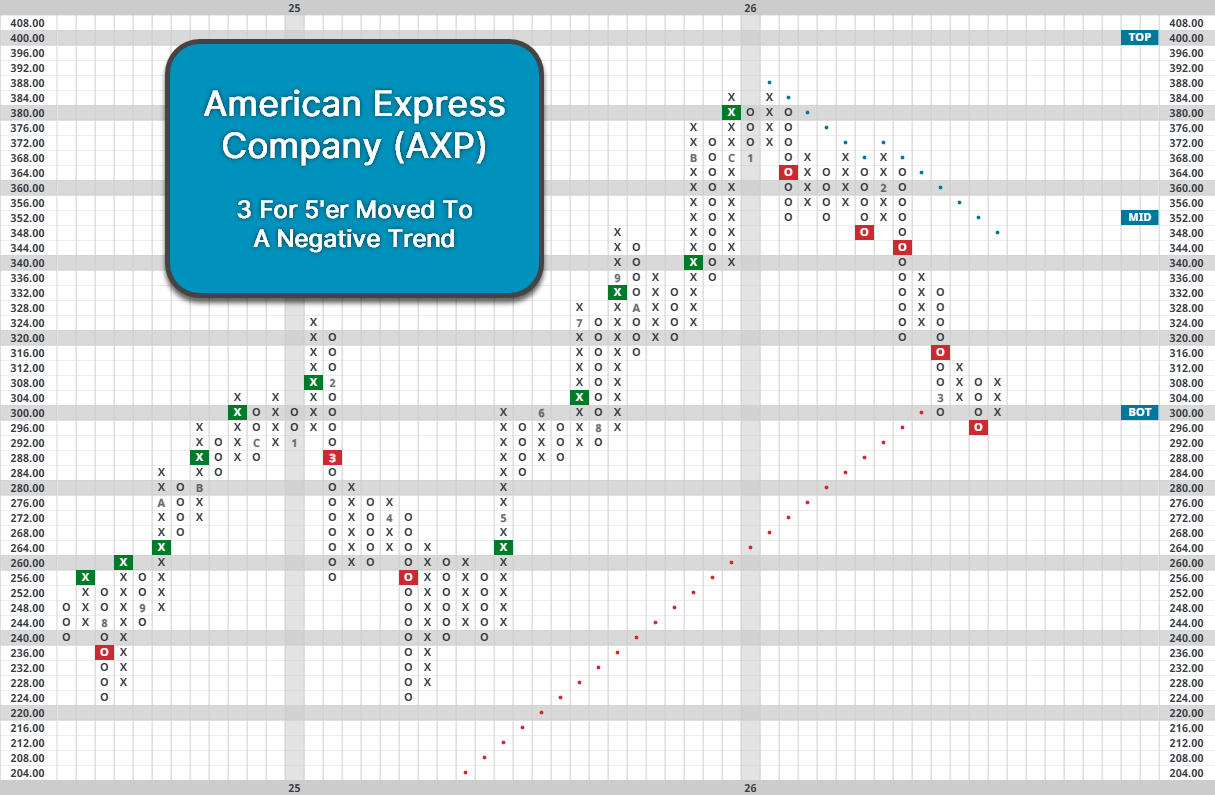

One financial area we previously highlighted as experiencing weakness was payment processors, whose movement often coincides with expectations of consumer spending. While the subgroup has been disrupted by potential legislation limiting fees and interest charges, it has also fallen further due to lowered expectations of consumer spending, even among the higher tax-bracket demographic. Last year saw significant discussion about the “k-shaped” US economy in which businesses and the upper class continue spending while the average American failed to enjoy the same benefits. Notably, American Express (AXP) was an exception to downside several months ago as its high-end customer base was made it resilient in the face of declines from Visa (V) and Mastercard (MA). However, the last couple months have seen it drop by 20% from highs, falling into a negative trend and moving down to hold territory as an oversold 3 for 5’er.

AXP’s selloff is partially due to the potential for AI‑driven white‑collar layoffs to dampen spending by its affluent customer base. When combined with potential business struggles and increases in credit risk, there are some initial signs that the upper branch of the k-shaped economy is starting to slow down. If financials truly are a reflection of the economy and its potential deceleration, then the sector deserves more attention in the coming months as the economy continues to navigate uncertainty. Regardless of what might be driving the sector lower, the relative strength of the sector has undoubtedly been headed in the wrong direction of late, even if it remains in ok territory for the time being.