The market has found a new narrative to rally behind—and it’s shying away from the very thing that previously led it higher: AI.

The market has found a new narrative to rally behind—and it’s shying away from the very thing that previously led it higher: AI. As artificial intelligence continues to advance, so too does its disruption of established companies. While the market is roughly flat on the year, there has been a lot of movement beneath the surface of domestic equities, with each of the top nine sectors in DALI changing from the start of the year.

One popular explanation for recent rotation within domestic equities is the HALO (hard assets, low obsolescence) trade, a term coined by Josh Brown of Ritholtz Wealth Management. The term refers to investors leaving companies at risk of being replaced by AI while moving to companies involved with hard assets whose business operations can’t be easily replaced by LLM‑driven automation. Consequently, the HALO trade has been a tailwind for capital intensive sectors as investors rotate into them and away from areas disrupted by AI.

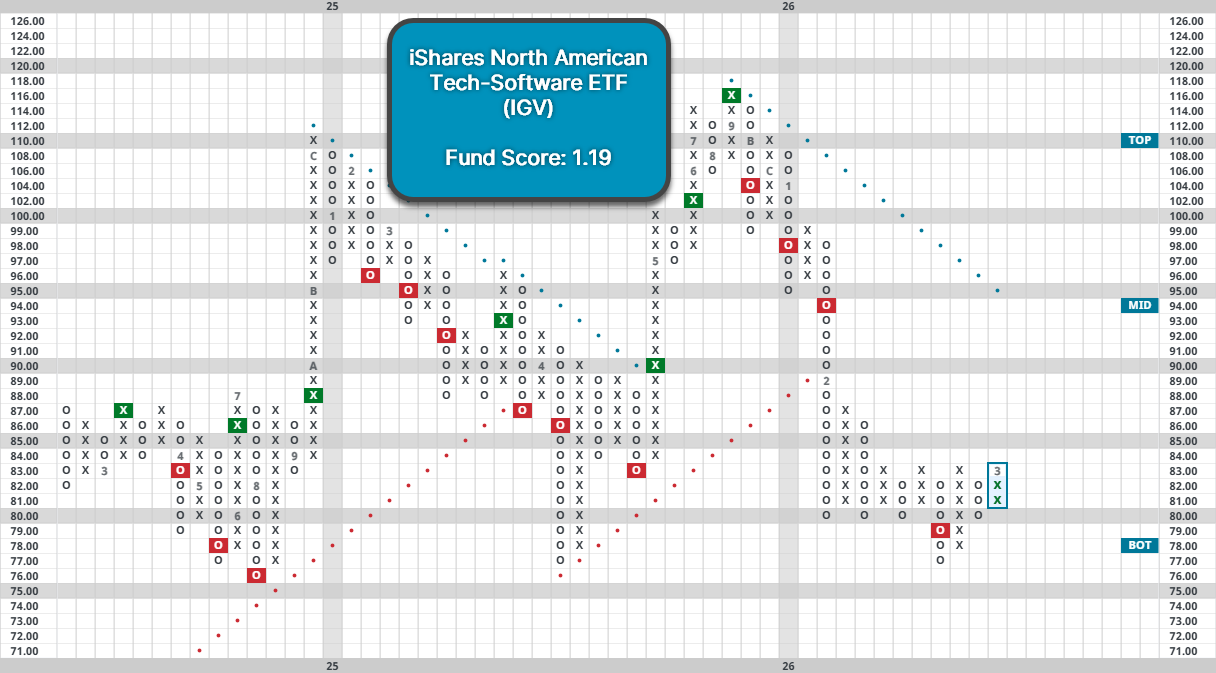

No area has been impacted by AI more than software companies, which have sharply declined over the last several months as investors worry about their longevity in an AI-dominated landscape. These concerns intensified following last month’s release of Claude’s Cowork tool, seeing software fund IGV fall another 10% in February as it sits more than 30% below its late‑2025 high. Meanwhile, its fund score is down to an abysmal 1.19 after being as high as 5.76 several months ago. However, not all areas of the market have seen this same level of disruption, even within technology.

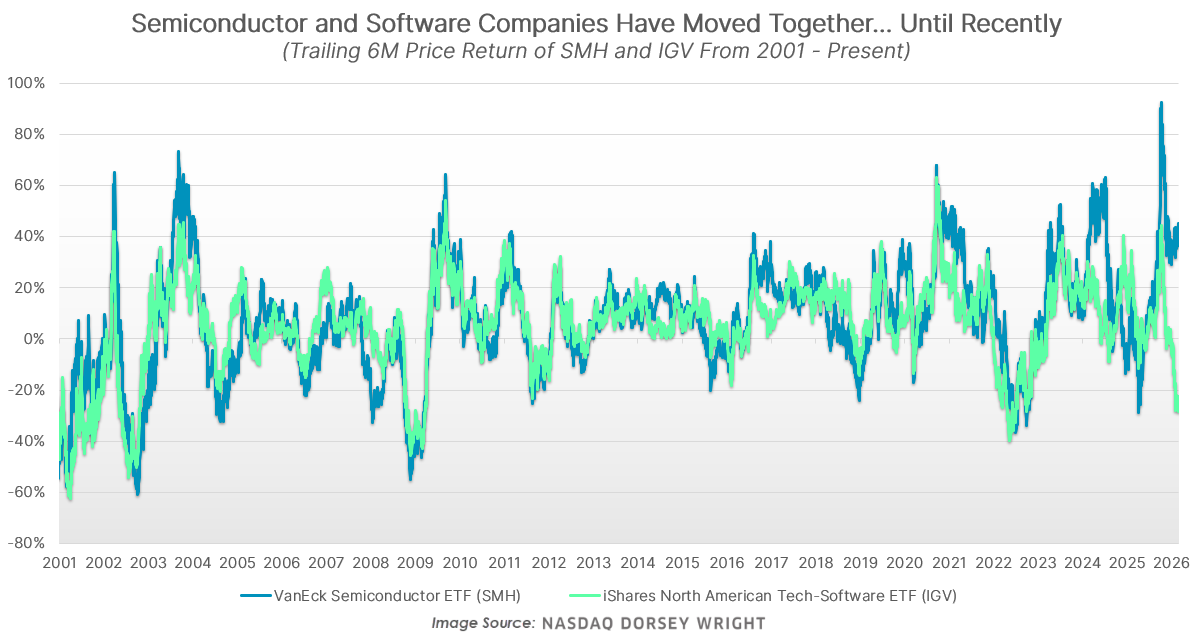

Notably, semiconductors have been relatively immune to the weakness of software companies. The VanEck Semiconductor ETF (SMH) set new highs late last month and displays a near-perfect fund score of 5.87. Over the last six months, SMH has gained an extremely solid 36.5%, whereas IGV has plummeted a whopping 24%. The more than 60% spread between the two technology groups is the widest going back to at least 2001, marking a extremely unusual departure from historical norms. Unlike software, AI development continues to be a huge benefit for the broader semiconductor industry, potentially justifying its much greater relative strength and outlook.

Despite semiconductor companies’ best efforts, technology no longer sits in the top three spots of DALI as investors look to other areas. Taking the place of Technology and Communication Services at the top have been Industrials, Energy, and Basic Materials, respectively. Additionally, those three are the best performing major sectors when looking at SPDR funds YTD. The rise of these sectors marks a stark contrast with prior leadership dominated by mega cap tech and growth companies. In fact, Industrials, Energy, and Basic Materials now have a total of 571 tally signals in DALI, which is their highest mark in several years and close to their most of all time. Looking at similar environments of strength for those three sectors draws parallels between our current environment and 2021/2022 as well as the mid-2000s. While both of those periods preceded some eventual market downside, every market environment is unique, so we shouldn’t put too much stock in those instances with domestic equities holding up well for now.

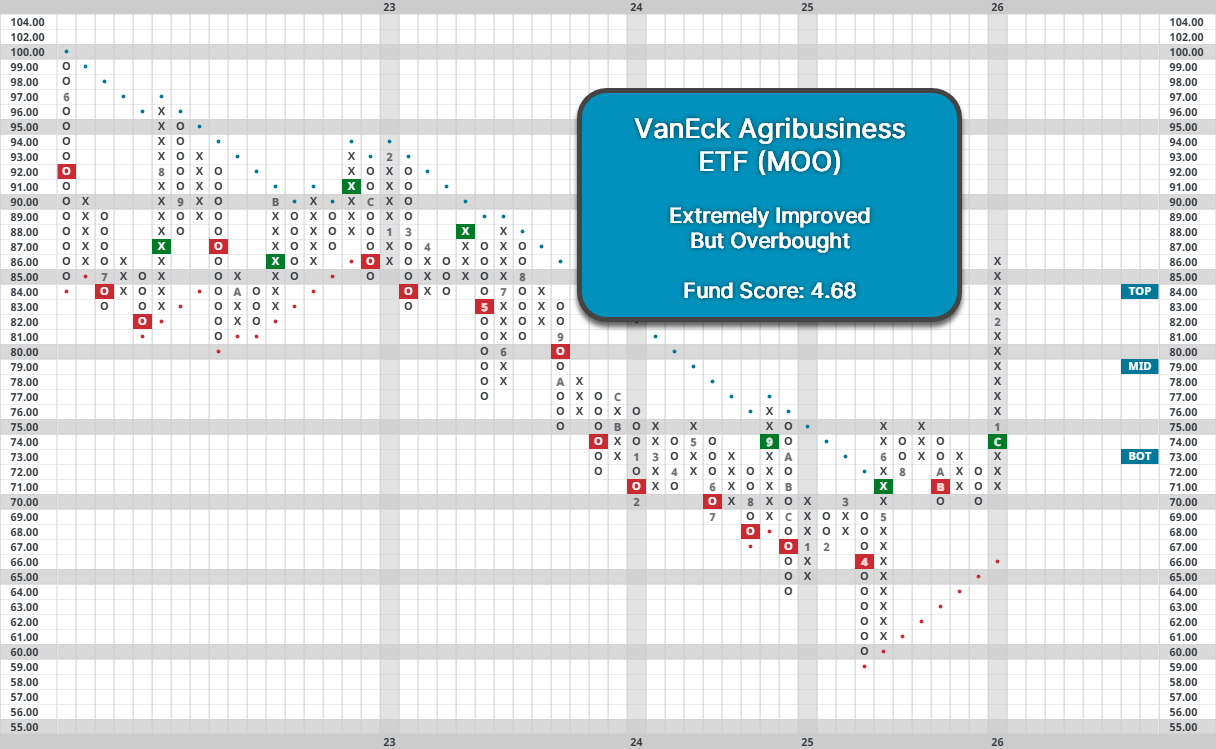

Staples have also benefited from their irreplaceability in the same regard as many of the “heavy asset” sectors. The State Street Consumer Staples Select Sector SPDR ETF (XLP) is the fourth best performing sector this year. Within Staples, food and agriculture companies have done even better, with the VanEck Agribusiness ETF (MOO) up 17.6% YTD with a solid fund score of 4.68. Recent movement has left it somewhat overbought, so those investors seeking to buy should wait for a pullback or consolidation. Those looking to diversify into HALO areas could look at Staples or any of the three previously mentioned sectors, especially if the groups continue to gain further strength.

The development of AI is still in its early stages, and there continues to be a high level of uncertainty surrounding its impact in the coming years. However, it’s encouraging to see strength within domestic equities broaden outside of mega cap technology. A market not dependent on its largest names is a healthier one, and old economy areas could keep the market moving higher even if further AI disruption continues.