The Fed has embraced a “data dependent” approach when it comes to making policy decisions and with a CPI release Tuesday morning, it’s a good time to see where the data stands.

Last week we discussed the market’s expectations and the Fed regarding monetary policy. In short, the market was expecting rate cuts to begin early next year and strong odds the Fed Funds rate would be cut by at least 100 basis points by the end of next year. However, the Fed has reiterated the need for interest rates to remain high until inflation drops back to its 2% target. The Fed has embraced a “data dependent” approach when it comes to making policy decisions and with a CPI release Tuesday morning, it’s a good time to see where the data stands. Last week it was mentioned that any data showing signs that the Fed may need to hold rates higher for longer than the market expected would likely be bad for assets, especially bonds which were coming off one of their best monthly performances in decades and already in extended territory.

Digging into this month’s CPI data, the overall direction of inflation is still lower but was not as encouraging as many were expecting. The YoY percent change for All Items ticked lower thanks mostly to declining energy prices with the MoM change coming in at 0.1%. However, outside of energy prices, most major categories moved higher with the less volatile All Items Less Food and Energy posting a YoY change of 4% and a MoM change of 0.3%. In the grand scheme of things, most of the data still shows that inflation is on a path to head back down to the 2% target. Aside from energy prices taking a major downtick, food prices have moderated with a MoM reading in October of 0% and a November reading of 0.1%. Shelter costs remain a thorn in the Fed’s side, however, the shelter reading has notable lagging components that go into its calculation, so that is something to keep in mind. To reiterate, this wasn’t a bad print for the general trend of inflation heading lower, however, it wasn’t as strong of a print as we’ve seen either and market expectations have shifted on the news.

With respect to market expectations, last week it was mentioned that market participants were pricing in a 60% chance the Fed made an interest rate cut by March, those odds are now down to 40% (CME). Not an extreme change, but not something to scoff at either. Getting back to a point made earlier, energy prices were a major contributing factor to headline inflation only showing a slight increase of 0.1% rather than closer to the ex-food and energy number of 0.3%. Much of the decrease in energy prices can be attributed to a clearer picture of the conflict in Israel as well as weak economic numbers coming from places like China and Europe stoking demand concerns. However, crude oil is now trading below $70 again for the first time since July. The mid-60s have been a support area for crude oil this year, so further downside, at least to the extent we’ve seen since October, may be harder to come by. While energy has been a big boost to lower inflation numbers, those gains shouldn’t be counted on to continue given where Crude Oil (CL/) is trading. Also mentioned last week, the market shrugged off initial news from OPEC+ regarding more supply cuts, however, OPEC+ has shown a willingness to take measures to defend prices, especially at these levels. For example, Saudi Arabia announced a voluntary cut in June this year when crude oil was trading at around $70 per barrel.

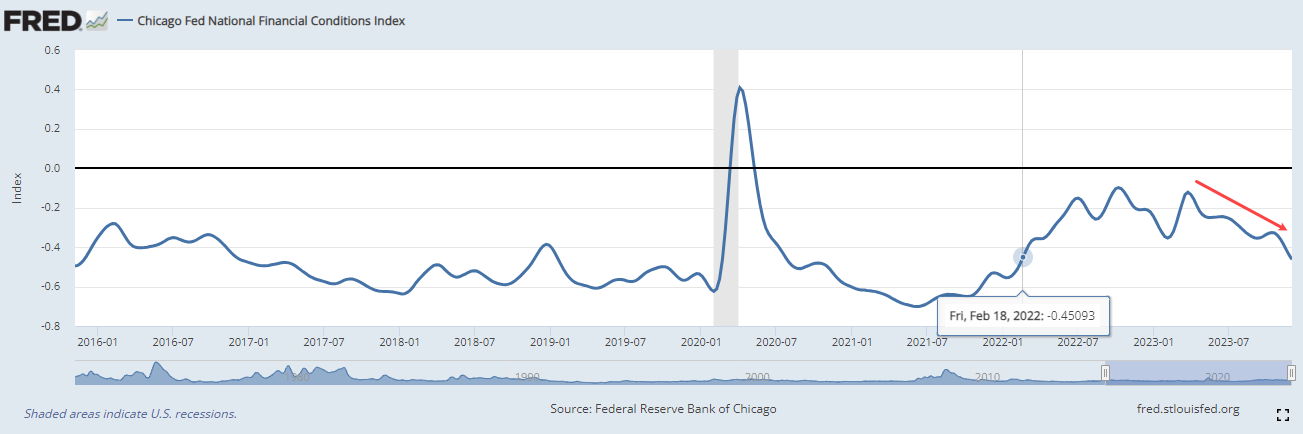

Not shown in the CPI data, the Fed keeps track of financial conditions. One of the main ideas behind raising interest rates is that it tightens financial conditions thus leading to less economic activity and lower inflation. However, according to the Chicago Fed’s National Financial Conditions Index, financial conditions have loosened consistently since March and are now the loosest they’ve been since February 2022. This can be seen in the chart below; negative readings signify financial conditions are looser than average while the opposite is true for positive readings. The most recent dive lower is likely due to interest rates falling since October as market participants began pricing in interest rate cuts early next year. Paradoxically, the market expecting lower interest rates has created a reason for interest rates to stay higher for longer. Due to loosening financial conditions as the market expects lower interest rates are soon on the horizon, the Fed is now forced to try to tighten financial conditions through policy or rhetoric.

At this point in time, it seems still unlikely that the Fed has another rate hike up its sleeve but it can say it won’t cut interest rates noting that financial conditions have loosened. Wednesday’s FOMC meeting will potentially shed some light on the Fed’s outlook given the looser financial conditions and the market’s expectations for rate cuts. Inflation data continues to show a general decline albeit at a slower pace than many expected from the data this morning. Energy prices were the biggest contributor to a low headline number, but continued downside may be difficult to come by as crude oil approached long-term support. Overall, the market hasn’t changed its view too much on the expectation of multiple rate cuts next year, but it has pushed them out further with Tuesday’s CPI data.