Interest rate policy has been at the forefront of investors’ minds for years and has only been exacerbated by the aggressive hiking the Federal Reserve has done since early 2022. Market participants seem to not only think rate hikes are behind us, but that the Fed will cut rates substantially next year.

Interest rate policy has been at the forefront of investors’ minds for years and has only been exacerbated by the aggressive hiking the Federal Reserve has done since early 2022. Market participants seem to not only think rate hikes are behind us, but that the Fed will cut rates substantially next year. A useful tool to see market expectations of the Fed Funds Rate is through the CME’s FedWatch Tool (link here). The tool allows users to see the probabilities being priced into changes in the Fed Funds Rate at different meeting dates. The first rate cut is likely to take place in March with a 62% chance the Fed Funds Rate will be lowered at that meeting. Looking further out, the market is pricing in more than a 90% chance the Fed will cut rates by at least 100 basis points by December 2024. While most market participants expected the Fed to begin cutting rates next year, expectations have shifted dramatically over the last month. Referring to March, the market has priced in over a 60% chance the Fed cuts rates. A month ago, the odds of a rate cut in March were only 25%. This massive shift is a bit perplexing when just looking at economic data and statements from Fed officials. Inflation is still above 2%, but growth is strong and while the Fed has suggested that rate hikes are over it has held the line that rates will need to stay elevated so that inflation can return to the 2% target. Nonetheless, the market doesn’t believe rates will stay higher for longer despite the “positive” data. It should be noted that rate expectations could dramatically shift in the other direction as well, elevators can go up as well as down.

Other assets have moved in a way that backs up the rate cut expectations as well as a less positive economic backdrop. One example is gold which hit a new all-time high above 2100 on Sunday night when futures began trading. It has since pulled back to a little over 2000 (not displayed on the chart below). The volatility in the precious metals space is a bit confounding but gold has been trending higher since October, undoubtedly helped by changes in rate expectations. While gold may be more rate-oriented in its moves, oil has started to show signs of a weakening economic backdrop. The most telling was oil’s reaction to OPEC+’s production cut announcement last week in which it struggled to catch a bid. One of the factors that contributed to the lack of upside is the doubt that OPEC+ participants will adhere to the cuts. However, another reason for the struggle for oil prices to move higher is economic concerns. While economic data has been perceived as positive or neutral for the most part in the US, the global picture is much less favorable. China has been a major issue and European data has started to turn downwards (Investing.com). Overall, some of the largest commodities markets are signaling the expectation of lower interest rates and less economic activity.

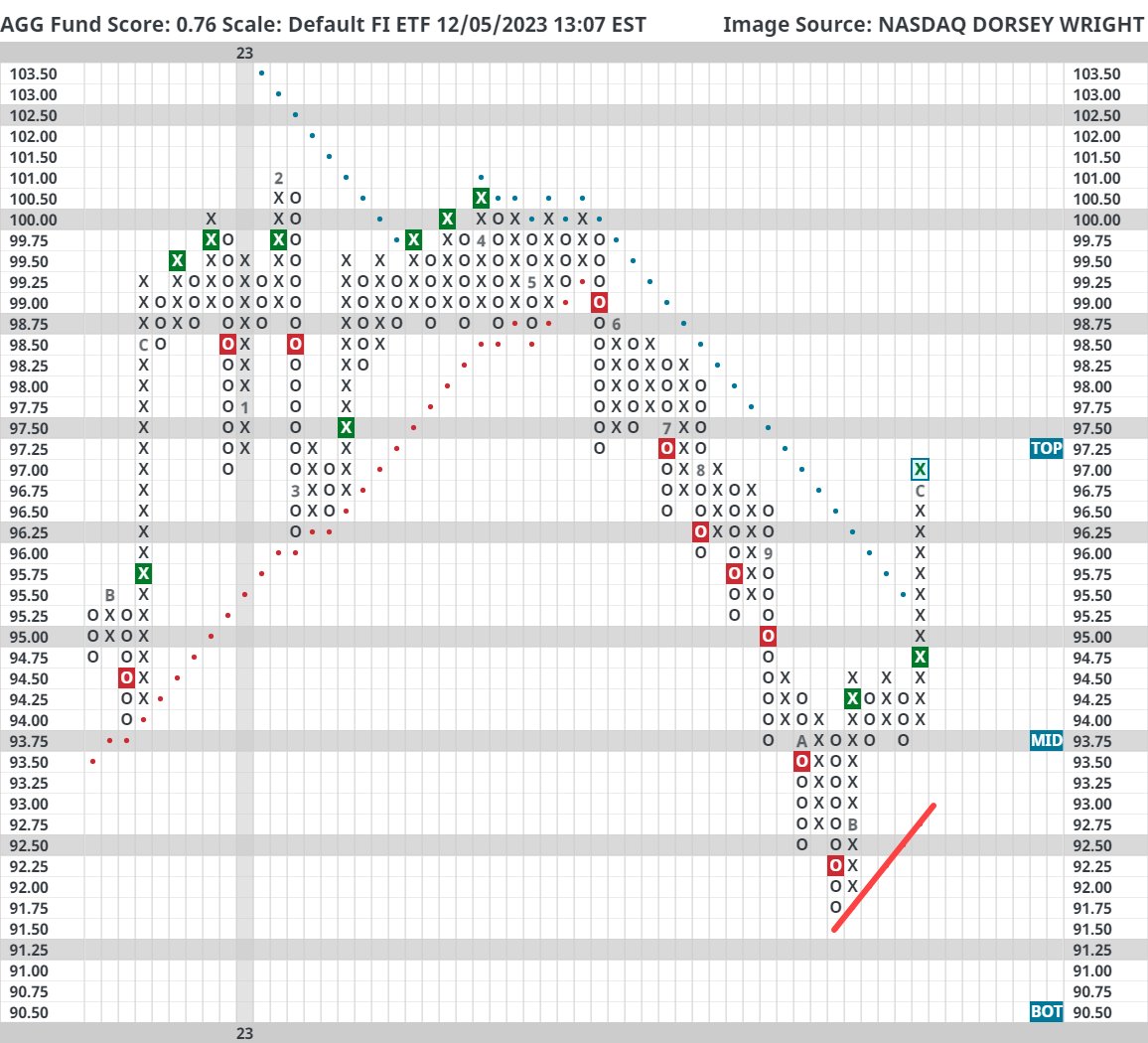

Lastly and most directly associated with rate expectations has been the improvement in the fixed income market. The iShares US Core Bond ETF (AGG) has gained 5.23% since putting in a recent bottom on October 19th. The S&P 500 Index (SPX) has gained 6.82% over the same period, a notable underperformance from a risk-adjusted basis. On top of a strong performance over the last month and a half, AGG now trades on two consecutive buy signals and recently entered a positive trend for the first time since May. AGG still has a poor fund score of 0.76 but bonds have caught a significant bid that shouldn’t be ignored. As is the case with outsized moves, AGG now sits at the top of its trading band with a weekly overbought/oversold reading of 75%, its highest reading since July 2020, and lacks support until $93.75. While there may be some short-term headwinds because of the current posture, bonds are looking like they’re turning a corner for the first time in a long time.

In conclusion, the price action across multiple asset classes as well as what’s being priced into the Fed Fund futures market shows that despite positive or lukewarm US economic data, investors are expecting a drawdown in economic activity and not believing the Fed’s current story. The price action in the bond market is the biggest marker of a shift in sentiment. However, equity markets seem unbothered by some of these developments for the time being as the S&P 500 Index is within shouting distance of its all-time high. Nonetheless, the move in bonds and commodities shows that the market has been going through changes underneath the surface. Moving forward, it’s important to stay alert on any more developments as we close out 2023.