Semiconductors now take up almost half of technology's weight within the S&P 500 and are now larger than 10 of the 11 broad sectors.

Technology has been a growing sector within the S&P 500 over a decade. At the end of 2016, Information Technology made up just 13.53% of the S&P 500, as of the end of April this year it now makes up 34.97% of the index. Within Information Technology, there are four GICS industries: Semiconductors, Software, Technology Hardware Storage & Peripherals, and Electronic Equipment Instruments & Components. A decade ago, software, hardware, and semis each made up 3-4% of the overall S&P 500. Through second half of the 2010s and first four years of the 2020s, software was the biggest gainer, moving from 3.99% to over 10% by the end of 2023. Both hardware and semis followed suit albeit to a lesser extent. Starting in 2022, semis began a consistent ascendancy, more than tripling their size within the S&P 500 in less than four years, going from 5.05% to 16.67%. If semiconductors were their own broad sector, it would be larger than every other sector except for technology. Furthermore, semiconductors make up more of the S&P 500 than the energy, consumer staples, utilities, real estate, basic materials, and communications combined. With our data through the end of April, semis are even larger than displayed in the chart below. The iShares Semiconductor ETF (SOXX) is up 15.37% (not including the 5% intraday gain during the time of this writing) in May while the SPX is up just 3.37%.

Drilling further into the weight of each industry in the information technology sector, we can see how dominant semis have become within the broader sector. Semiconductors now make up just under half of the technology sector, more than doubling since the launch of OpenAI’s ChatGPT at the end of 2022. Besides an increase from software’s share of the technology sector in 2018, the four industry groups had been in balance until 2022. While semis have increased their intrasector weighting significantly, software and tech hardware have been the biggest losers. Electronic equipment, by far the smallest portion of the tech sector, has stayed at roughly the same level over the last decade.

*Note that the weightings do not add up to 100% due to lack of industry level data for some stocks*

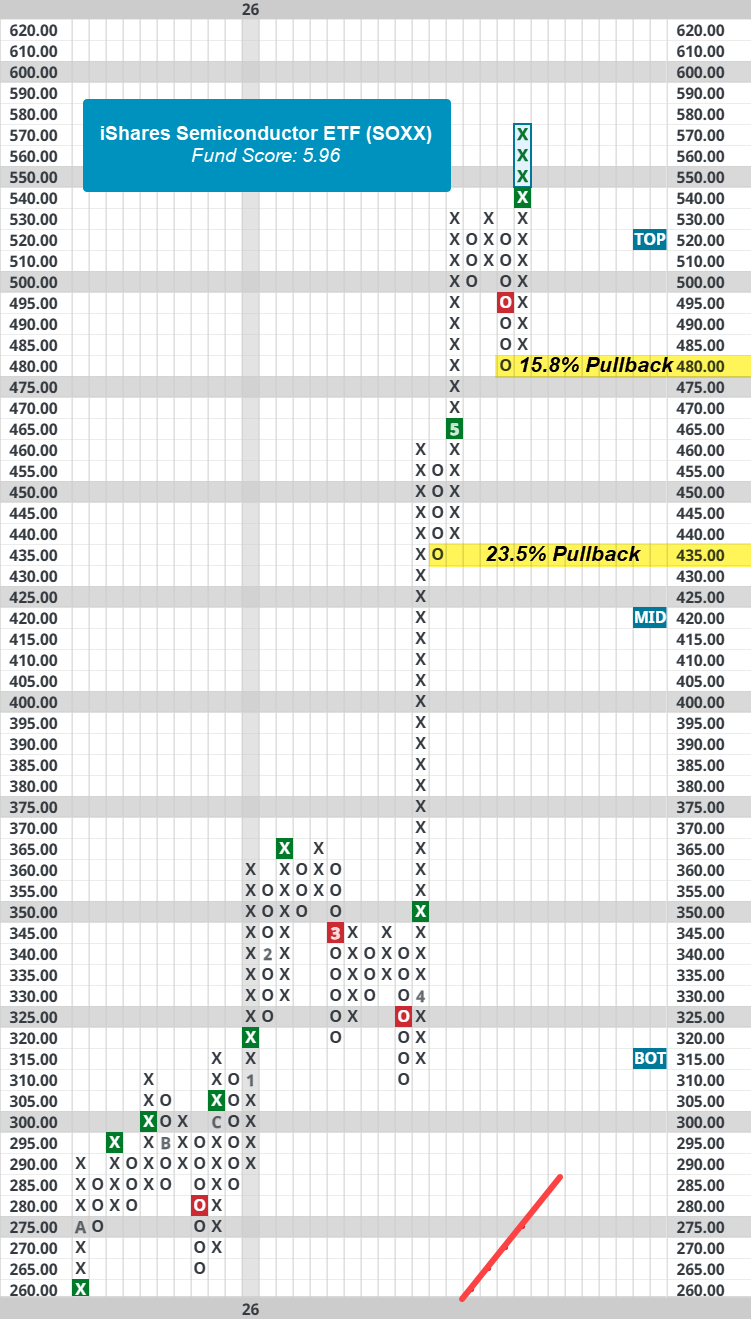

In short, semiconductors are in the driver’s seat for the technology sector and have a greater impact on the market than every other broad sector. Looking at semis’ technical picture via the iShares Semiconductor ETF (SOXX), the fund has a near-perfect 5.96 fund score, recently completed a shakeout pattern, and reached a new all-time high today. With today’s move, SOXX has an intraday weekly overbought/oversold reading of almost 150%, near the highest level ever. To say price action is frothy in the short term would be an understatement. Nonetheless, with a near-perfect fund score, it’s hard to be bearish on SOXX except for the possibility of a pullback in a greater uptrend. However, a pullback could be uncomfortable as the fund is about 15% away from its nearest support level which was established last week. In any case, it would be prudent to look through any direct exposure to the sector via ETFs like SOXX or individual equity names to consider trimming exposure or putting in some stops so a large pullback won’t be detrimental to unrealized gains.