We examine the hypothetical performance of buying the S&P at all-time highs since 1980.

In Wednesday’s trading, the S&P 500 (SPX) hit a record high for the 16th time this year. As investors, we’re generally happy to see the market hitting new records. However, if you have money sitting on the sideline watching the market push relentlessly higher while you’re not fully invested can be nerve-racking. We’ve been trained “buy the dip”, “buy low, sell high” so putting money into the market when it’s trading at all-time highs can feel like a bit of a sucker’s bet. After all, a better buying opportunity will surely come along before too long, right?

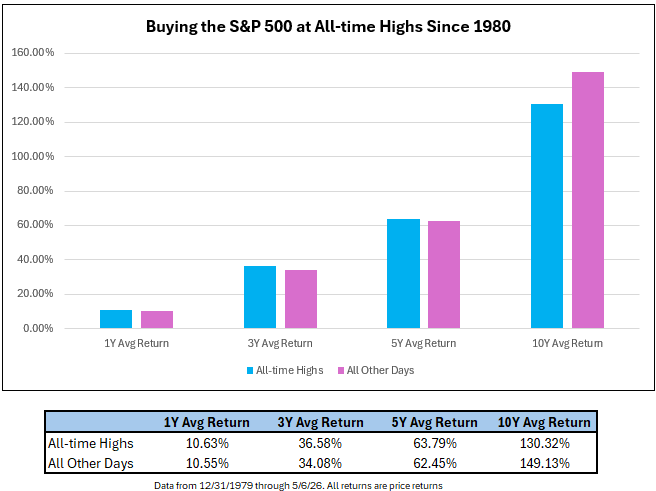

There is a lot of “common wisdom” in this business, some of it good, some of it not so good and until you start doing some analysis, it can be hard to tell, which is which. So, what about the notion that we shouldn’t buy into a market that’s trading at an all-time high? In order to test this idea, we looked at every trading day since the beginning of 1980 and divided them into two categories – days the market hit a new all-time high (based on intraday high) and days that it didn’t. We then calculated the one-, three-, five-, and 10-year forward returns for each day and averaged them. The results are shown below.

As you can see the results of our study show that over the intermediate-to-long-term buying all-time highs isn’t detrimental to overall returns. In fact, buying on days the market hit a new all-time high outperformed the average for all other days over the one-, three-, and five-year periods. Over the 10-year period, buying all-time high days outperformed buying other days, but the difference was relatively modest at 130% vs. 149%

Of course, some will still wonder, why would you buy the market at all-time highs when the 10-year average return is better for all other days? But what this argument overlooks is that the time in the market that is sacrificed, especially if waiting for a meaningful pullback. The S&P 500 hit its first all-time high after the Q1 slide on 4/15, and since then it’s gained an additional 4.9% through Wednesday’s (5/6) close. Two weeks ago, we discussed the merits of going all-in versus averaging into positions and found that, generally, it’s better to go all-in instead of hedging your bets by averaging into exposure. There is a common theme between this study and that one – time in the market typically works in your favor, even if you’re entering at a time when the common wisdom says the market is “expensive.”

As discussed in yesterday’s report, one of the major (perceived) pitfalls or criticisms of momentum strategies is that they often buy assets that are trading at or near record highs. The results of this study are also clear counterpoint to that criticism as over the last 45+ years, buying the S&P when it’s trading near all-time highs has produced strong returns over the intermediate- and long-term.