Commodities have fallen down to third as precious metals have cooled and energy bounces back and forth amid unrest in the Middle East. We discuss the change today.

Seemingly as quickly as it went up, Commodities have fallen down into the third position within the NDW DALI rankings… but perhaps not quite for the reason many would have anticipated. With continued unrest in the Middle East over the last few weeks, energy focused names have driven up towards the top of the rankings, seeing the likes of crude oil and other areas of the energy complex reach levels not tested for a handful of years. The swift nature of the supply shock saw many representatives move into heavily overbought territory on their default charts, leading lots of recent commentary to site the possibility for normalization in the near-term as the situation surrounding the ongoing conflict continues to develop. Energy prices generally fell on Monday (3/23) as news surfaced of further delays in US strikes of key facilities after there had been some apparent progression in talks to end the conflict. While it is certainly still too early to tell if this is genuine progress in de-escalation or just a bluff from President Trump, crude oil fell as much as 12% from this weekend’s highs to cool off in the low $90’s. There is obviously still plenty of room for continued volatility in the near-term, but any news of progress will likely continue to send energy lower.

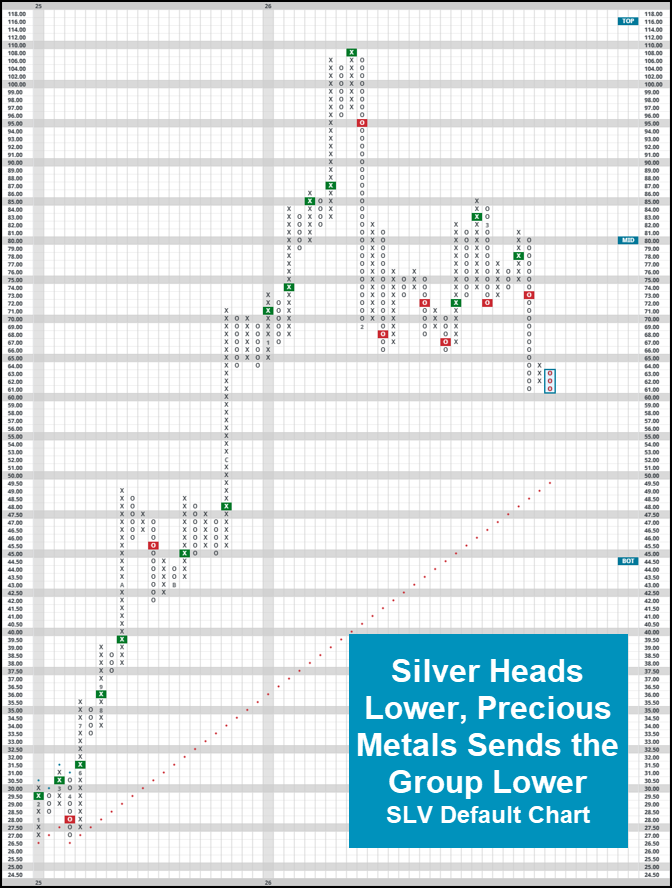

While further declines in energy names would undoubtedly yield further deterioration for the commodities group within the broad rankings, the group was not the main driver of Monday’s move lower within the overall DALI rankings. Precious metals have suddenly struggled quite mightily, seeing the likes of silver (SLV, -4.5% YTD) or gold (GLD, +4.5% YTD) trade well off 2026 highs. While both funds maintain strong fund scores, there is no question that things have technically deteriorated and it isn’t the time to just blindly buy into the space like we might have been able to do throughout 2025. SLV, included below, returned to a column of O’s with intra-day action on 3/23, putting in a localized level of resistance below a major level of support in the mid-$60’s. Now trading for roughly half of the levels we saw during the meteoric rise earlier in the year, there is certainly cause for a bit of concern in the near-term.

To close today’s piece, we will refocus on the DALI rankings. With the updates to the rankings on Monday’s morning, commodities lost 40 signals in a single day as major representatives for the space returned to RS sell signals against other areas. For reference, the 40-signal drop is the largest single day decline in signal count for the group since the start of our data in 2002 and represents a roughly 15% decline in total signals. While there could certainly be further volatility in store, the move confirms some (relative) strength for both domestic and international equites. The move also highlights the need for a process in following the rankings- waiting for a major signal landmark (10-15 signal difference) before making broader shifts or waiting until the end of the month can help prevent whipsaw and confirm strength in one direction or the next.