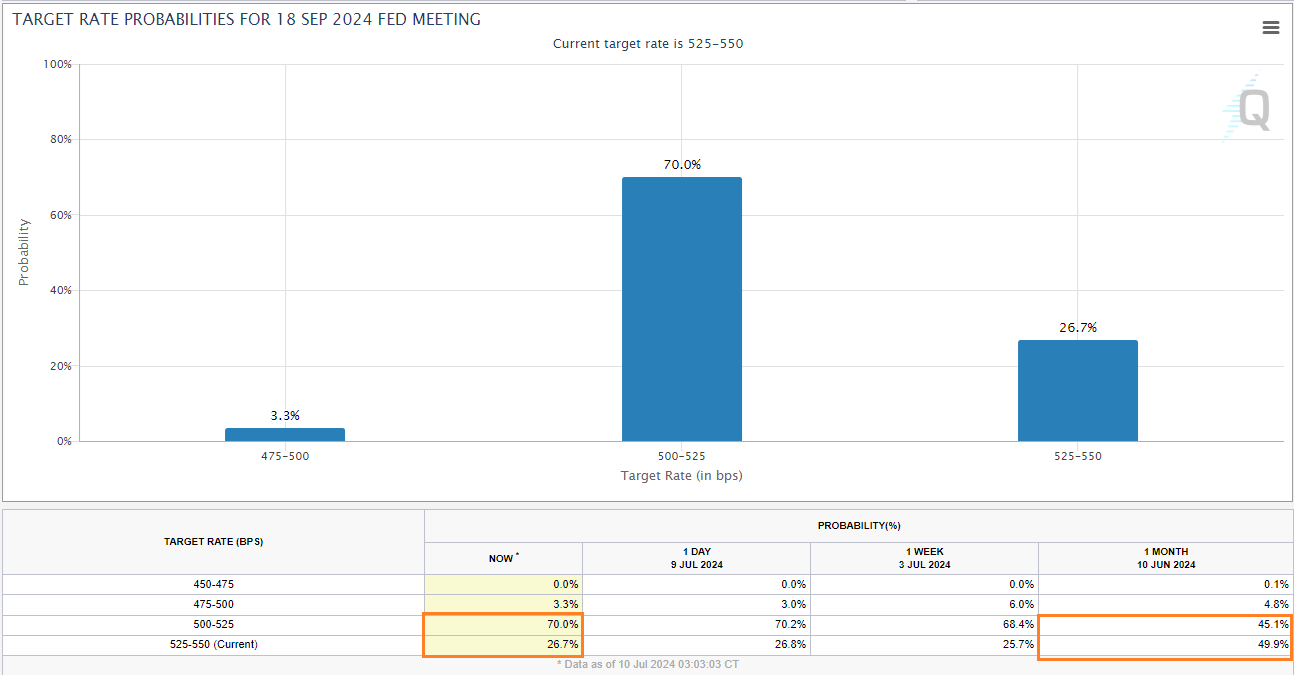

US Treasury yields were down over the last week. The fed futures market is now pricing in a better than 70% chance of a 25 bps cut at the September meeting.

Weekly Fixed Income Update Video (2:50)

US Treasury yields were down over the last week and the US Treasury 10-year Yield Index (TNX) remains on two consecutive sell signals but has thus far maintained its positive trend. The June jobs report released last Friday showed that the unemployment rate had ticked up to 4.1%, raising expectations that the Fed will cut rates.

The fed futures market is now pricing in a better than 70% chance of a 25 bps cut at the September meeting. A month ago, those odds stood at right around 50%. The market is also pricing in a better than 70% chance of two rates cuts by the end of the year.

Although most areas of relative strength within fixed income remain outside the core, over the last few weeks we have seen improvement in some core groups. US Government-Agency is on the verge of crossing above the 3.0 score threshold for the first time since January. While investment grade corporates and general bond-long groups have crossed above the 2.5 threshold.

If the market continues to expect easing from the Fed, putting downward pressure on long-term rates, we are likely to see to see these groups continue to improve. We’ll get our next look at inflation on Thursday with the release of the CPI report. Another downtick in inflation would bolster the case for the Fed to lower rates.