The past week saw no significant technical developments in the Technology, Basic Materials, Consumer Non-Cyclical, Healthcare, Energy, Financials or Real Estate Sectors. Those that saw noteworthy movement are included below.

U.S. Sector Updates

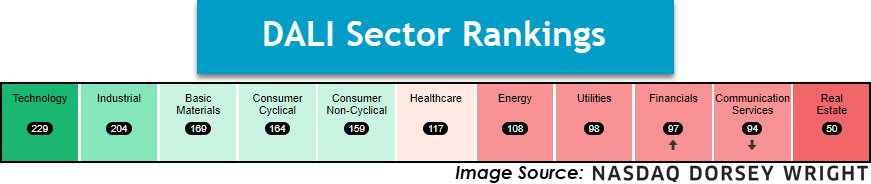

The past week saw no significant technical developments in the Technology, Basic Materials, Consumer Non-Cyclical, Healthcare, Energy, Financials or Real Estate Sectors. Those that saw noteworthy movement are included below, in order of their relative strength ranking in the DALI domestic equity sector rankings. Sector designations are based on DALI sector rankings and are as follows: 1 - 3 overweight, 4 - 7 equal-weight, and 8 - 11 underweight.

Industrials- Overweight

Industrials maintain the 2nd spot with the broad rankings this week, lagging only Technology by just over 20 buy signals. The pair have separated themselves nicely from the rest of the pack and continue to flex their muscles from a returns perspective. XLI holds a strong fund score and continues to march higher this week but is close to reaching overbought conditions at the time of this writing. Underneath the hood, the sector is picking up from an earnings perspective. A big loser this week was Raytheon (RTX) which tumbled on the news of a slew of engine recalls. Consider moving out of this technically unacceptable name into another one from the sector, that being Boeing (BA). The stock moved to new 52-week highs on reports of strong operating cash flows. BA is an actionable 3/5’er at current levels.

Consumer Discretionary – Equal Weight

The Discretionary Select Sector SPDR Fund XLY was down 2.6% over the past week, but the fund has still yet to reverse into Os on its default chart. From here, a reversal would come with a move below $170, and we would look for the fund to continue to consolidate at current levels. Pulte Group PHM is a homebuilding name that might not get as much attention as its counterparts, DHI and LEN, but the company reported earnings yesterday and beat expectations. While most homebuilders have had revenues retract year-over-year, PHM saw a roughly 8% increase compared to Q2 2022. The stock is a 4 for 5’er that ranks in the top decile of the Building sector matrix and is currently trading at all-time highs. PHM is actionable on a pullback toward $80. Notable earnings upcoming are Ford F, Comcast CMCSA, and McDonald's MCD reporting on 7/27; Norwegian NCLH, Marriot MAR, and Starbucks SBUX reporting on 8/1.

Utilities – Underweight

Utilities perked up this past week with XLU adding 4.32%. On the more sensitive 0.50 point per box chart, XLU did return to a buy signal and move back into a positive trend, but the fund still hasn’t shown the same improvement on its default chart. Earnings for the sector begin in earnest on 7/27 with PG&E PCG, a 5 for 5’er in the sector trading near multi-year highs, along with American Electric Power AEP and Centerpoint Energy CNP all reporting on Thursday. Edison International EIX joins the aforementioned three, while First Energy FE will report next week on 8/1.

Communication Services- Underweight

Communication Services slumped back into the 10th position of the DALI rankings this week, but it should be noted that the fall comes from the close race for signals in the bottom half of the rankings rather than overarching weakness from the sector as a whole. Several names are on the docket for earnings this week, including Alphabet (GOOGL & GOOG) which jumped on strong results, and META which reports after close on Wednesday. DIS continues to be a name to avoid, now within earshot of 2023 lows and on a string of consecutive sell signals. Comcast (CMCSA) is a more traditional communication name you may consider for exposure to the media subsector.