We compare domestic equity industry performance in political environments with a unified government controlling the executive and legislative branches against a divided government.

The first full week of 2021 saw major domestic equity indices continue higher, as shown by the S&P 500 Index SPX posting its second straight week of gains at a return of 1.83% through Friday. This came after residents of Georgia completed a runoff election from November that resulted in the Democratic party gaining two additional senate seats, which will effectively give the Democratic party control of the Senate when factoring in the tie-breaking vote of Vice President-elect Harris. Combining these results with the November election results indicates that the Democratic party will be in control of both houses of Congress and the White House for the first time since 2009. The 117th Congress that began in 2021 marks the 24th occurrence of a single party controlling both Congress and the White House since 1926. Interestingly enough, this is equal to the number of times we have seen a division of power between the White House, Senate, or House of Representatives. With domestic equity markets starting the year at or near all-time highs, there has been no shortage of speculation around how we should expect markets to perform with this new political environment.

In order to help provide perspective on what we might expect, we have reexamined the sector data that we looked at for our Presidential Election study in November. Recall that this looked at the historical performance of 10 broad domestic equity industry sectors using data pulled from the Ken French Data Library. This is the same Ken French from the famous Farma-French Model. This data was used as it ran from December 1926 through December 2019, allowing us to take our testing back significantly further than what is offered by the current GICs sectors. A breakdown of what is included in each of the ten industries can be found below:

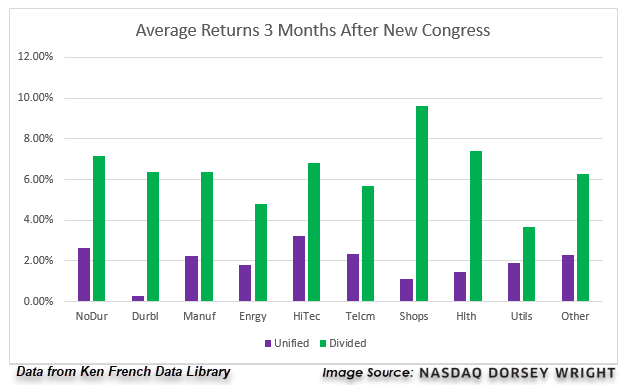

Using these sectors, we then took the average returns of each portfolio over a forward 3-month, 6-month, and 12-month timeframe beginning at the start of each new Congress since 1927. These average returns were then further separated out by whether or not we had unification or division among the political parties in power of the executive and legislative branches. The results of each industry’s forward returns are below, along with some observations. Note that these industry indices are market-cap weighted and use total return data.

- The first quarter of a new congress sees lower average returns across the board if there is a unified party in power.

- Each of the industry groups still manages to average positive returns in the first three months of unified leadership.

- Durables and Shops show the lowest average returns in unified governments during this timeframe.

- The best performing industry in this timeframe for unified governments is HiTech.

- Returns increase significantly six months after a new congress, with each industry posting an average gain of at least 4% regardless of the political environment.

- The leading sectors of a unified government over a forward 6-month timeframe include HiTech, Utilities, and Durables.

- Healthcare and Telecom are among the lagging sectors.

- The industry breakdown changes substantially 12 months after a new congress, with 8 out of the 10 groups showing higher average forward returns with a unified government than with a divided one.

- Durables and HiTech continue to lead the way for unified governments, with Manufacturing and Energy picking up the pace to also be among the leaders.

- Telecom, Utilities, and Non-durables are the laggards from a 12 month forward return aspect.