Several long-term bond funds gave sell signals last week, while one corporate bond fund returned to a buy signal.

Although there has been little or no movement on the charts of the major US yield indices, there were a handful of sell signals on the charts of medium and long-term bond funds over the last week.

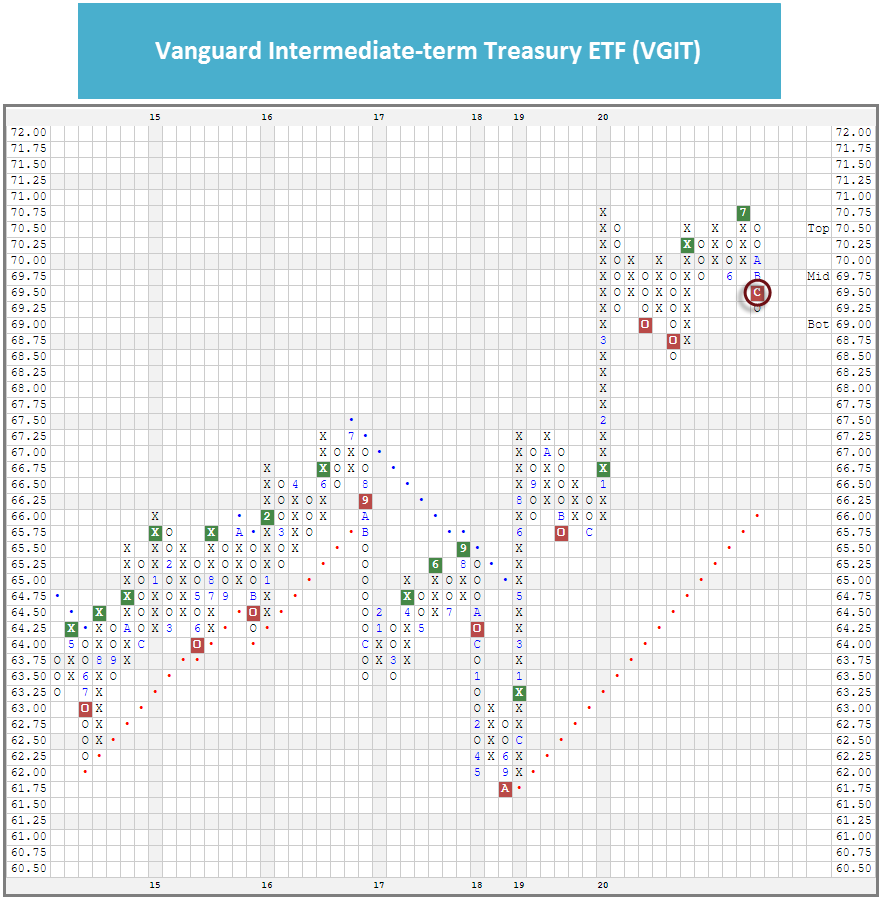

The Vanguard Intermediate-term Treasury ETF VGIT broke a triple bottom at $69.50 last week, taking out support that had been in place since March. VGIT currently has an unfavorable 1.99 fund score and a negative -3.28 score direction. From here, the next level of support sits at $68.50.

The iShares Barclays 10-20 Year Treasury Bond ETF TLH also returned to a sell signal last week when it broke a double bottom at $157.50. TLH currently has a 1.60 fund score and a negative -3.41 score direction. TLH’s next level of support sits at $157.

Finally, the Vanguard Long-term Bond ETF BLV broke a spread quad bottom at $109, taking out support that dated back to September. BLV currently has a 2.33 fund score and negative -2.00 score direction. Its next level of support sits at $106.50.

Since the beginning of November, the score of the US Fixed Income Long Duration group in the Asset Class Group Scores has declined from 0.4 points from 3.36 to its current level of 2.96.

Interestingly, while the intermediate- and long-term bond fund mentioned above each gave sell signals last week. The iShares iBoxx $ Investment Grade Corp. Bond ETF LQD returned to a buy signal on 12/24 when it broke a double top at $137.75.

We quite often see investment grade corporate bonds make similar directional moves to US Treasuries as they also tend be sensitive to changing interest rates. However, while Treasury yields have risen over the recent term, US corporate bond spreads (the difference in yield between corporate bonds and Treasuries) has narrowed further, mitigating (or perhaps even outstripping) the effect rising yields has had on corporate bonds.

One possible explanation for this is that the bond market interprets the recent news about COVID-19 vaccines as a positive for the US economy and thus expects that, at some point the Fed’s monetary policy will tighten, resulting in higher Treasury yields. Meanwhile, a stronger economy means that corporate borrowers are less likely to default and thus investors demand less of a premium to hold corporate bonds over US Treasuries, driving down corporate spreads.