Following Thursday’s (5/28) action Technology ascended to the top spot within the NDW Sector Rankings with much of the recent gain in relative strength coming from software.

Following Thursday’s (5/28) action Technology ascended to the top spot within the NDW Sector Rankings – gaining four additional buy (tally) signals and overtaking Energy. Through May, the State Street Technology Select Sector ETF (XLK) has added another 17%, outperforming the S&P 500 (SPX) and the remaining ten sector SPDR funds by more than 13% (4/30/2026 – 5/28/2026). Unquestionably, leadership within the sector is still focused within semiconductors, but the broader sector’s improvement over the past couple of months has brought it from 5th to 1st. Additionally, the notable performance divergence within the technology sector witnessed earlier this year between semis and software, the sector’s laggard subsector, has narrowed.

Among the relative strength relationships involving broader sector representation to see a change in signal this week were the State Street Technology Select Sector ETF (XLK) versus the Invesco S&P Equal Weight Energy ETF (RSPG) and the Invesco S&P Equal Weight Technology ETF (RSPT) versus the State Street Energy Select Sector ETF (XLE) on a 3.25% scale. XLK reversed back into Xs against RSPG following Tuesday’s (5/26) trading and returned to an RS buy signal after action on 5/27. RSPT switched back to a column of Xs and returned to an RS buy signal following Tuesday’s (5/26) action. In both cases, the RS charts had been in a column of Os briefly earlier in May and on an RS sell signal since March. It is worth noting that the 3.25% scale RS charts between XLK versus XLE is within two boxes of an RS buy signal, while the RSPT versus RSPG RS chart is within one box of an RS buy signal. The overall theme with these RS charts shows the broader sector’s superior relative strength against the now second place sector and market darling from earlier this year, energy.

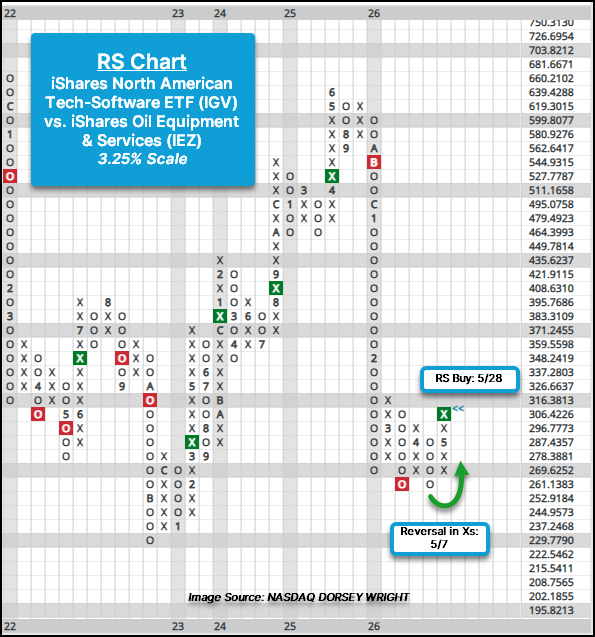

Along with the broader sector RS changes for broader technology this week, what had been a laggard subsector for the broader market, software, is now showing superior RS against the leading energy subsector, oil equipment and services. The 3.25% scale RS chart of the iShares North American Tech-Software ETF (IGV) versus the iShares Oil Equipment & Services ETF (IEZ) reversed into Xs earlier this month and returned to an RS buy signal following Thursday’s (5/28) action. Prior to the recent RS signal flip, IGV had been on an RS sell signal since November 2025.

This change in relative strength for the software space has been the primary driver behind the broader technology sector’s recent ascension as IGV has been the biggest buy signal contributor to technology’s buy signal within the DALI sector rankings in the month of May. With much of the broader technology space rally to new highs and potentially residing in overbought territory, those seeking exposure are either going to look for consolidation or look to subsectors that have improved recently, like software, to provide slight diversification to potentially concentrated exposure within semis.