A common question we get from clients is if momentum has been doing well, then should I look to rotate out of the factor?

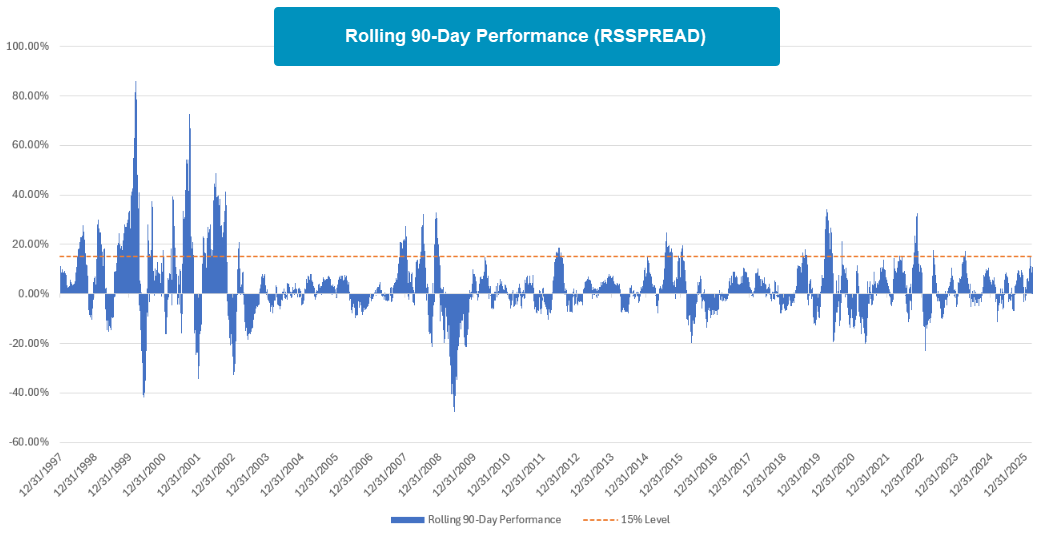

A common question we get from clients is if momentum has been doing well, then should I look to rotate out of the factor? To try to answer that question, we first need to find a measure for the current state of momentum. One measure would be the RS Spread Index (RSSPREAD) which looks at the difference in performance between a basket of high-momentum names versus a basket of low-momentum names. If the RS Spread Index is moving higher, then the high-momentum names are performing better than the low-momentum names and vice versa. Using the RSSPREAD, we looked at the rolling 3-month performance of the index with reading above 15% being considered “hot” momentum markets. While there have been periods that have well exceeded 15% (tech bubble era, GFC, and covid), it is an acceptable line of demarcation in “normal” market environments.

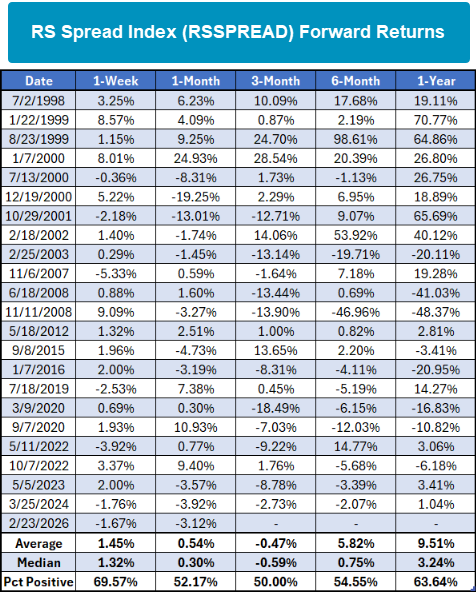

Now that we have a measure for “hot” momentum markets, let’s look at how momentum strategies fair moving forward. As a first look, the performance of RSSPREAD following a 15% gain over the last three months should give a decent indication of how momentum strategies fair moving forward. The table below breaks down the results. We’ve removed clusters within three months to look at first occurrences only. RSSPREAD tends to continue to push higher on short-term and long-term time frames, however, the three-month period was rough spot compared to the other time periods observed. Even though the average and median numbers were slightly negative over the three-month period, it was not material enough to say that it’s worth rotating out of momentum strategies. This is especially the case when looking at the one-year numbers.

While RSSPREAD may give us the indication that momentum strategies can continue to do well following a strong momentum backdrop, it is not a directly investible asset. To remedy this, we’ve looked at the performance spread between the Invesco Nasdaq Dorsey Wright Momentum ETF (PDP) and the S&P 500 Equal Weight Index (SPXEWI). On average, PDP outperformed SPXEWI over each time frame observed but this outperformance becomes more muted when looking at the median. The percent positive metric is typically sticky around 50%, so it’s a coin flip whether PDP outperforms SPXEWI over the observed time frames. At worst, there appears to be no clear indication that momentum strategies will suffer after a strong run. To get back to the original question, if momentum has been doing well, then should I look to rotate out of the factor? There’s not much evidence supporting rotating out of momentum following a good performance window in the long run.