Over the past several years, betting on the market broadening beyond mega cap growth names has generally meant leaving upside on the table—until recently. Will the average stock fall behind again, or will this time truly be different?

Over the past several years, betting on the market broadening beyond mega cap growth names has generally meant leaving upside on the table—until recently. The Nasdaq-100 (NDX) has outperformed the S&P 500 Equal Weight (SPXEWI)—representing the average S&P 500 stock—by a cumulative 86.8% since the start of 2023. In contrast, SPXEWI has outperformed NDX by 11% since the end of October, highlighting the abnormality of recent market behavior. Given these developments, will the average stocks fall behind again, or will this time truly be different?

One sign of optimism comes from the performance of the average stock versus the Nasdaq-100 and the Invesco QQQ Trust (QQQ) fund that tracks it. The S&P 500 equal weight regained near-term relative strength over QQQ for the first time since the summer of 2024, underscoring the resurgence of the “average Joes” compared to growth stock giants.

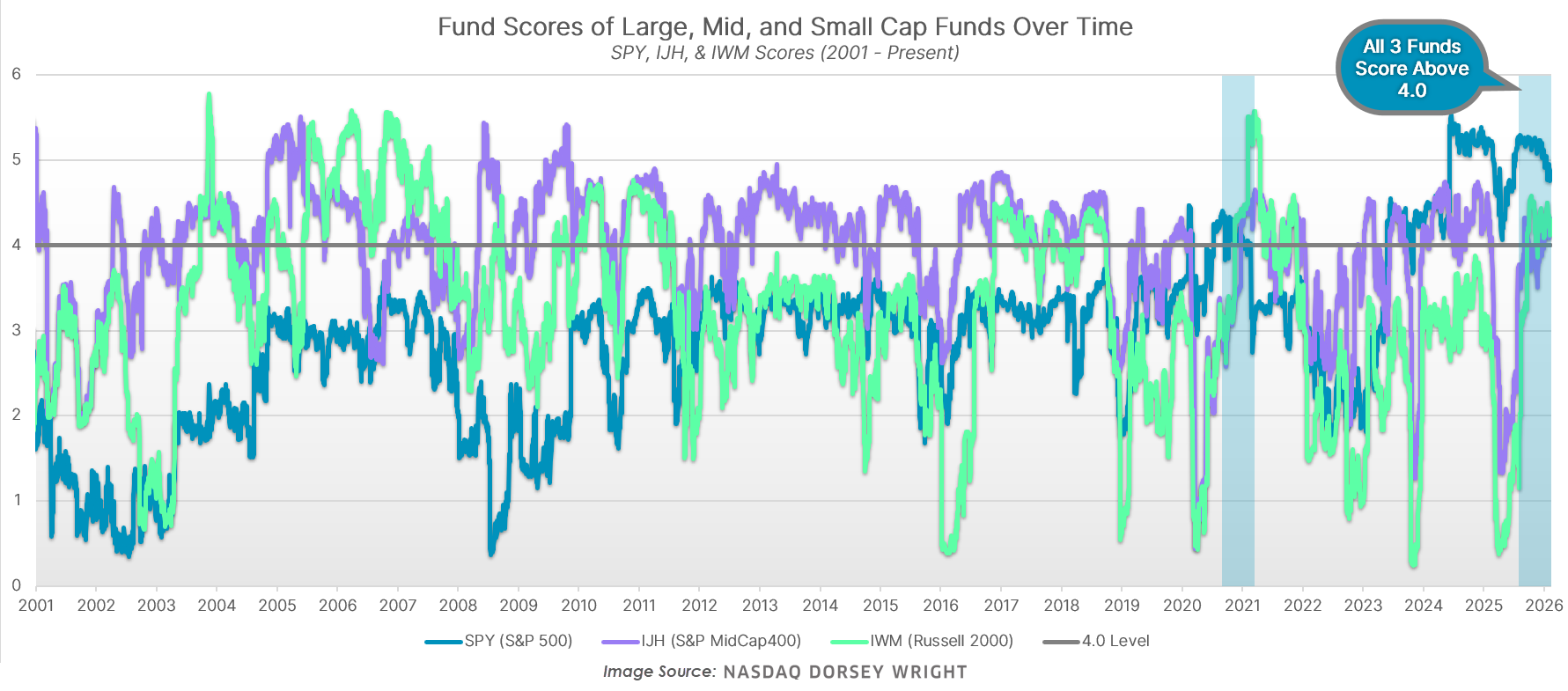

Moreover, recent gains have been sharpest outside of large caps. The iShares S&P MidCap 400 Index Fund (IJH) and iShares Russell 2000 ETF (IWM) are both handily beating the S&P 500’s 8.9% gain over the last six months, rising 14.9% and 20.3%, respectively. Sustained broad-based strength has resulted in SPY, IJH, and IWM all scoring above 4.0 for just the second time this century, with late 2020 being the only other recent instance.

Market broadening has also pushed participation within domestic equities to its highest levels in recent memory. Currently, the Bullish Percent for NYSE stocks (^BPNYSE) sits around 62%—its highest reading since late 2024. With more stocks and groups contributing to gains, market fragility should decrease as performance becomes less dependent on a handful of the largest names.

Strength has broadened not only across company sizes but also across the sectors leading the market. As noted in Monday’s report, only three of the eleven major sector SPDR funds managed to beat SPX the last three years. Conversely, recent gains have been driven by sectors beyond technology and communication services. Over the last three months, SPX has been roughly flat, yet eight of the eleven major sector SPDR funds have managed to beat the index.

Lastly, strength has broadened beyond just the US stocks market. Domestic equities sit several signals behind international equities in DALI’s asset class rankings, with commodities and fixed income also delivering solid performances over the trailing year. With so many different sizes, sectors, and asset classes pushing markets higher, continued broadening appears to be a defining theme of early 2026.

Given the widespread strength of financial markets, there appears to be less need for concentrated exposure in single groups like US mega cap growth—unlike recent years. Additionally, broader participation typically benefits trend‑following strategies, which can capitalize on more segments outperforming the benchmark, boding well for momentum as we look ahead to the rest of the year.