As we do each quarter, we will take today’s report to look across different asset classes and focus in on the best and worst performing funds for the 4th quarter and 2025 as a whole.

As we do each quarter, we will take today’s report to look across different asset classes and focus in on the best and worst performing funds for the 4th quarter and 2025 as a whole. Note, during our screen we filtered out leveraged and inverse funds & put in minimum volume and AUM requirements to focus solely on those funds you are most likely to see come across your desk. We also did our best to avoid similar kinds of funds when possible, (to avoid the entirety of our tables being taken up by silver, for example…) but there will likely be similar themes during our analysis.

We will start broadly by peering across all of the different asset groups at once. As you might expect, our top ten performers across both the 4th quarter and 2025 as a whole were littered with precious metals options. Outside of those groups, other international names (South Korea, Chile, Spain) found their way as top performers. Many of the worst performers came from names with large crypto exposure. Other full year underperformers came from dividend focused areas, which failed to keep up broader markets during what ended up being quite a productive year.

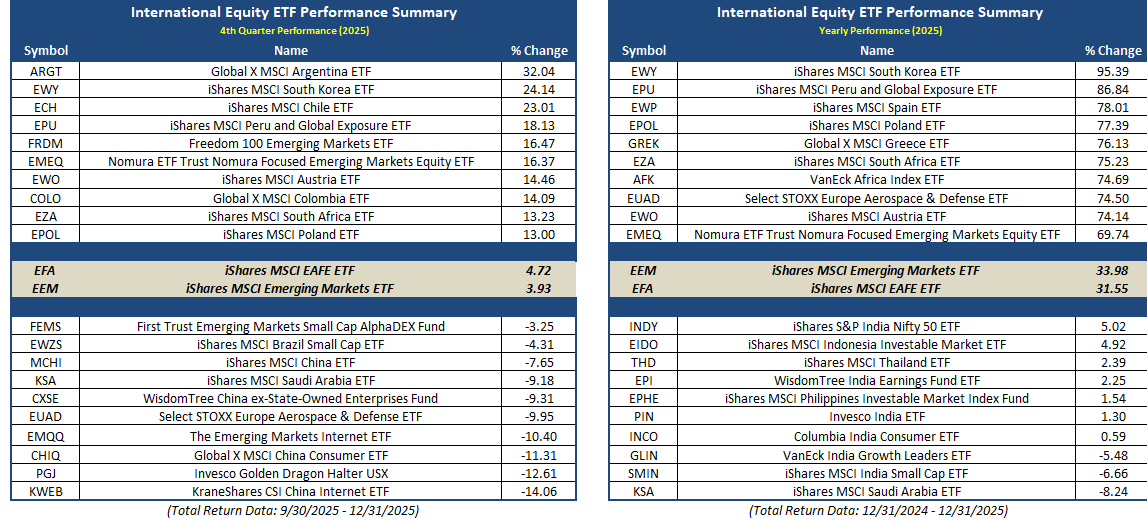

Speaking of international options, our table on the right dives underneath the hood of that group specifically. As mentioned previously, global options flexed their muscles throughout 2025, seeing major benchmarks put in constructive years against domestic markets. Points of interest come from a major performance bump in Q4 from Latin American names. China and India were major detractors from a pure performance perspective… but again its worth emphasizing both emerging and developed markets performed quite well in 2025.

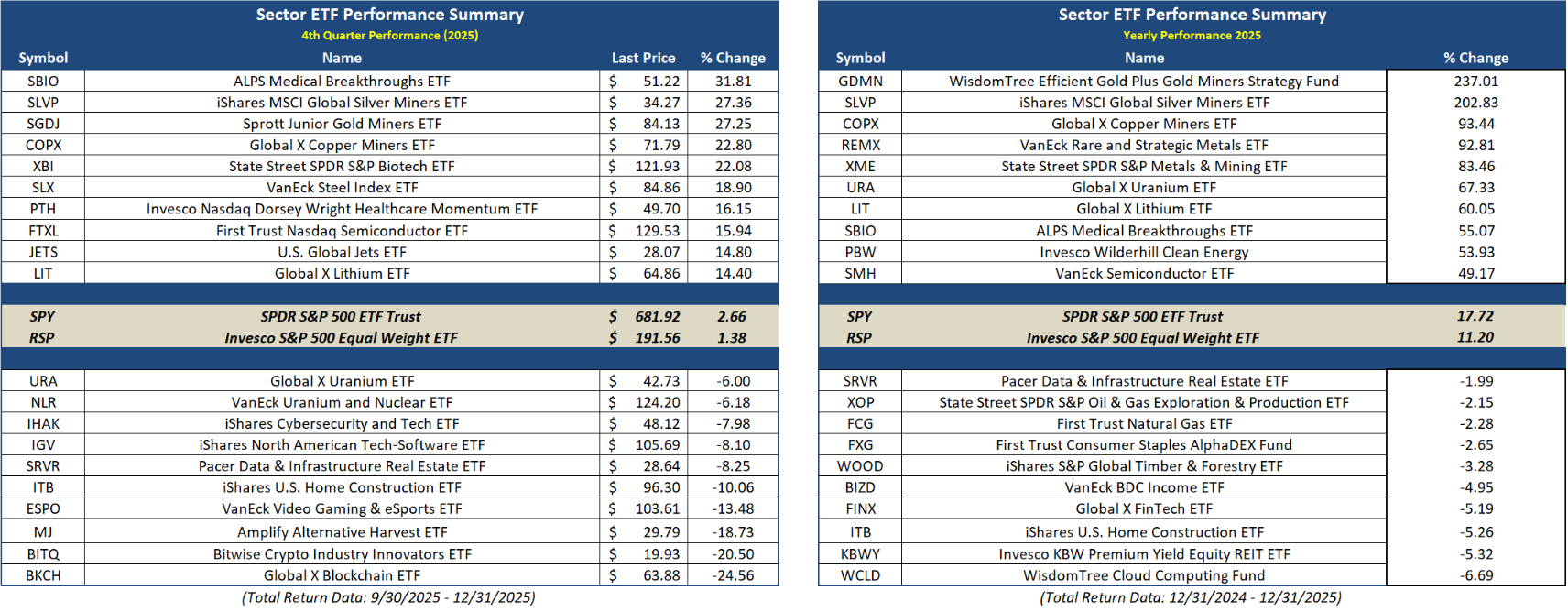

The following tables focus on individual sectors and commodities respectively. For the entire year, the top performers in 2025 are littered with strong precious metals and commodity focused areas. Of interest in terms of Q4 upside sector performers were healthcare options , materials focused areas, semis and airlines. Towards the downside, further lackluster returns came from the likes of crypto & real estate. Similar themes were present for full year results, adding in poor showings from energy representatives and consumer staples. On the commodities front, laggards came in the way of energy & agriculture- both groups remain points of relative weakness as we move into 2026.

Our last set of tables below detail performance trends for the broader fixed income and currencies space. While fixed income as a whole remains a laggard within our longer-term rankings, there were points of strength within the asset class heading into 2026. From a yearly perspective, risk-on options remain leaders as international and convertibles led the way in terms of their total return in 2025. Those themes held largely true throughout the 4th quarter. Underperformers for both the quarter and the year include longer-duration assets. Across the currency space, overall crypto names underperformed for both Q4 and the year as a whole. In terms of more traditional currencies, the US Dollar fell nearly 10% for the entire year… seeing other currencies appreciate against the greenback.