The seasonal market transition is a great time to evaluate your existing portfolio allocation. Today, we offer an idea that capitalizes on seasonal tendencies while maintaining a momentum focus at all times.

As of the close last Thursday (10/31), we ended the seasonally strong period and officially moved into the weak season of the market (May 1 – October 31). This year, in the “seasonally strong” period, the S&P 500 (SPX), Dow (.DJIA), and Nasdaq (NASD) each gained between 4% and 5.5%. Each of these major market benchmarks would have been in the red for that stretch were it not for the sharp rebounds seen in April. This marked the second straight year that the “strong” period underperformed the “weak” period immediately preceding it.

However, it isn’t easy to know when the market will buck a historical trend, and this is one of the reasons why we've put forth the concept of a seasonal "tilting" approach that employs factor investing. This is a way to incorporate a long-term, well-documented bias in the market, without resorting to an “all in or all out” strategy that many investors may find unpalatable. This strategy also offers an opportunity to further differentiate yourself within the wealth management space as an expert on investment factors.

Today, we will evaluate one of the seasonal portfolios that combines two momentum approaches while incorporating low volatility to ideally smooth out the ride over time. This is done by tactically shifting a portfolio's emphasis between the Invesco Nasdaq Dorsey Wright Momentum ETF (PDP) and the First Trust Nasdaq Dorsey Wright Momentum & Low Volatility ETF (DVOL) depending on the accompanying seasonal period. Since PDP is solely focused on momentum, it is the overweight fund during the “strong” seasonal period from November through April (70% PDP, 30% DVOL). The allocation then shifts to overweight DVOL during the “weak” seasonal period to provide more exposure to low volatility names (70% DVOL, 30% PDP). Even though both strategies focus on high momentum names, the low volatility screen used in DVOL has historically led to notable allocation differences. Combining the two approaches makes for an attractive US "core" equity solution.

This strategy is available under our Models page for platform subscribers to set alerts. Even though there will only be two trades a year, the website model can help with additional perspective or collateral needed before incorporating the strategy into your process. Remember, the point of any strategy won’t be (and shouldn’t be) to outperform every single year, but to create an all-weather portfolio that is systematic and defendable across various market environments.

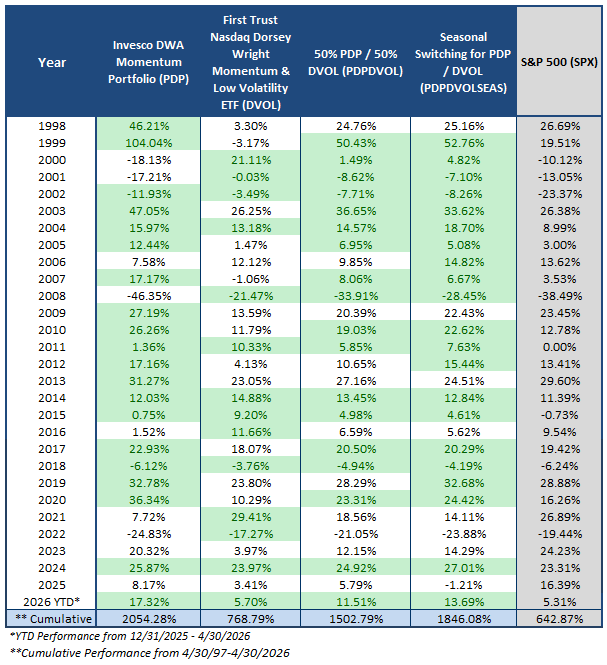

The table below shows the annual returns for each of the strategies, incorporating back-tested data prior to the launch of each fund. We also include some notable observations on the returns over the years.

Key Observations:

- Each strategy shows higher cumulative returns than the S&P 500 Index, despite not outperforming every year.

- Buying-and-holding PDP shows the highest cumulative return of any strategy, the largest single-year return of any strategy (104% in 1999), and the worst single-year drawdown of any strategy (-46% in 2008). While it is easy to gravitate to the largest cumulative number, knowing what it takes to arrive at that number is important.

- Combining PDP and DVOL in equal allocations leads to more favorable returns during turbulent market environments for momentum such as 2000-2002, 2008, and 2021-2022.

- Adding the seasonal switching overlay to the model leads to more consistent returns over time, potentially making the reigns easier to hold.

Disclosures:

Invesco Nasdaq Dorsey Wright Momentum ETF (PDP): https://www.invesco.com/us/en/financial-products/etfs/invesco-dorsey-wright-momentum-etf.html

First Trust Dorsey Wright Momentum & Low Volatility ETF (DVOL): https://www.ftportfolios.com/retail/etf/etfsummary.aspx?Ticker=DVOL

Performance prior to each funds’ inception date are back-tested and based upon the underlying index shown below:

Inception date of PDP is 3/1/2007, prior to that all testing is based on backtested strategy information available on the Dorsey Wright platform.

Inception date of DVOL is 9/5/2018, prior to that all testing is based on backtested strategy information available on the Dorsey Wright platform.

Returns for all models and benchmarks are Pure Price Returns, excluding dividends and transaction costs. Returns within the model portfolios are a result of back-testing. Back-tested performance is hypothetical and is provided for informational purposes to illustrate the effects of the strategy during a specific period. The hypothetical returns have been developed and tested by NDW, but have not been verified by any third party and are unaudited. Back-testing performance differs from actual performance because it is achieved through retroactive application of a model investment methodology designed with the benefit of hindsight.

Model performance data (both back-tested and live) does not represent the impact of material economic and market factors might have on an investment advisor’s decision-making process if the advisor were actually managing client money. Investors cannot invest directly in an index. Indexes have no fees. Past performance is not indicative of future results. Potential for profits is accompanied by possibility of loss.

The relative strength strategy is NOT a guarantee. There may be times where all investments and strategies are unfavorable and depreciate in value. Relative Strength is a measure of price momentum based on historical price activity. Relative Strength is not predictive and there is no assurance that forecasts based on relative strength can be relied upon