May marks the second seasonal evaluations for the Fund Score Method (FSM) models. As we do during each evaluation season, we will cover the trades and themes to get insights into any shifts in market leadership. Whether or not one follows any of the FSM models, their evaluations give us important information.

May marks the second seasonal evaluations for the Fund Score Method (FSM) models. If you’re not familiar with the FSM model framework, a large majority of the models evaluate their holdings on a seasonal quarter basis with February, May, August, and November marking the start/end of each seasonal quarter. Each FSM model is built around a universe of ETFs or mutual funds with the highest scoring funds selected at each evaluation. If you want a deeper dive into the basics for FSM models, check out our Fund Score Method Model Guide. As we do during each evaluation season, we will cover the trades and themes to get insights into any shifts in market leadership. Whether or not one follows any of the FSM models, their evaluations give us important information.

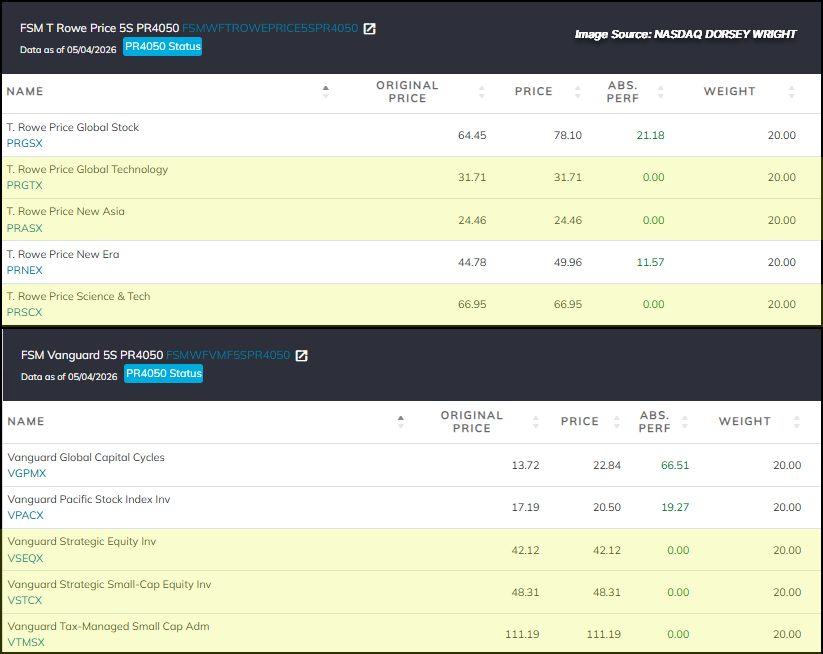

The major theme during the most recent evaluation for the FSM models witnessed a shift from models maintaining a notable overweight toward international equities to U.S. equity exposure. In some cases, the FSM models have seen their allocations go from entirely within international funds to more equal mix of international and domestic equities with slight overweight to one asset class present within certain strategies, depending on model universe makeup. The prime example of such shift comes from the T Rowe Price 5S PR4050 Model, which saw the removal of the Spectrum International (PSICX), International Value (TRIGX), and Overseas Stock (TROSX) funds, and the additions of New Asia (PRASX), Global Technology (PRGTX), and Science & Technology (PRSCX) funds. While the naming of the funds may signal more of an overweight toward international equities, the T Rowe Price 5S PR4050 Model’s underlying allocation of the individual stocks reveals a slight overweight toward U.S. equities, primarily within technology and energy.

The Vanguard 5S PR4050 Model witnessed a similar shift in asset allocation, but with a slight twist, as it removed the European Stock (VEURX), Developed Markets (VDVIX), and International Stock (VGTSX) funds and added the Tax-Managed Small Cap (VTMSX), Strategic Equity (VSEQX), and Strategic Small Cap (VSTCX). The addition of small caps brings the model to overweight U.S. equities along with exposure to the Pacific Stock (VPACX) and Global Capital Cycles (VGPMX) funds.

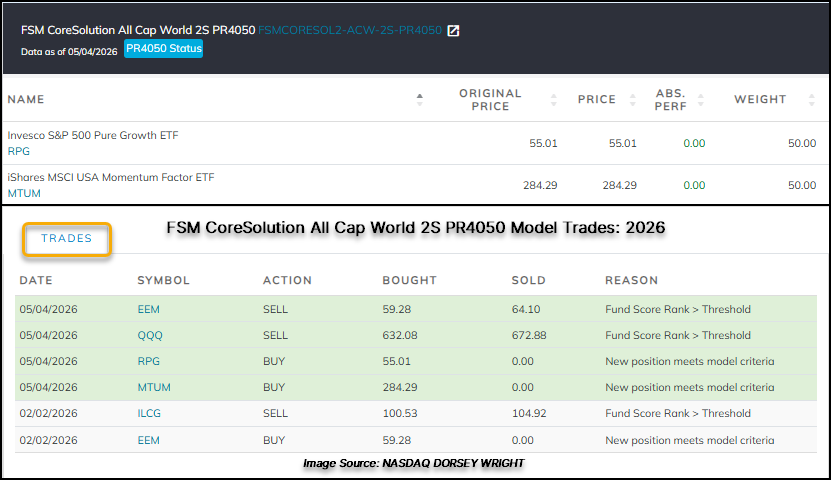

Within the CoreSolution lineup of FSM models, the FSM CoreSolution All Cap World 2S PR4050 followed the overall theme for the quarter – removing international and bringing in domestic exposure - and saw a complete turnover within the model. This seasonal quarter evaluation witnessed the removal of both the Invesco QQQ Trust (QQQ) and the iShares MSCI Emerging Markets ETF (EEM), while seeing the additions of the iShares MSCI USA Momentum Factor ETF (MTUM) and Invesco S&P 500 Pure Growth ETF (RPG). Along with the All Cap World 2S PR4050 Model removing QQQ, the FSM CoreSolution U.S. Core 2S PR4050 also removed the ETF while adding the SPDR S&P 500 Trust (SPY) in its place.

Though the notable theme for the quarter saw a shift from portfolios potentially overweight or entirely within international equities to either a more equal mix of international and domestic or slightly overweight toward domestic, the recent changes highlight both asset classes continuing to show superior trending and relative strength characteristics highlights the strength within the risk-on assets versus commodities and defensive assets.